Repair First or Document First After Property Damage? A Decision Framework for UAE Asset Managers

When property damage occurs, UAE facility managers, asset owners, and hospitality engineering leaders face a critical decision point: do we initiate immediate repairs, or do we secure comprehensive documentation first? For any incident that does not pose a direct threat to life or safety, the protocol is unambiguous: document first, then mitigate. Rushing into repairs without a verifiable, time-stamped record of the initial damage is the most common reason for insurance claim disputes and rejections in the UAE's compliance-driven commercial environment. The Critical First 60 Minutes: A Protocol for Asset Protection How your team responds within the first hour of discovering damage dictates the financial outcome for the asset. The natural impulse is to rectify the issue immediately. However, premature repairs can permanently destroy the evidence required by insurers to validate a claim. In the UAE, an absence of proof is often interpreted as an absence of grounds for a claim, potentially leaving your organisation with 100% of the liability. This initial phase is not about permanent fixes. It is about a disciplined, sequential response framework. Ensure Safety: Address immediate life-safety risks. This includes isolating water mains, de-energising electrical circuits, or evacuating the area. Personnel safety is the overriding priority. Document the Scene: Utilise mobile devices to capture detailed, time-stamped photographs and videos of the damage before any clean-up or repair work commences. Mitigate Further Damage: Only after evidence is secured, implement temporary measures to prevent escalation. This may involve deploying tarps over a leaking roof or relocating sensitive equipment from a flooded area. This "document, then mitigate" sequence separates a managed claims process from a financial liability. It establishes the clean, auditable trail that regional insurers and loss adjusters mandate. Financial Impact Analysis: Proceeding with repairs before documentation can result in claim denials of up to 100%. Insurers operate on verifiable evidence. Without a clear "before" state, they can argue the damage was pre-existing or less severe than claimed. Your initial documentation is your primary negotiating asset. The following framework provides decision-making clarity for on-site teams in the crucial first 15 minutes, prioritising actions based on damage type and associated risks. Immediate Action Protocol: A Risk-Based Framework Damage Scenario Immediate Priority (First 15 Mins) Justification (Primary Risk Factor) Indicative Response Time SLA (Industry Benchmark) Major Water Leak/Burst Pipe 1. Isolate water main. 2. Document source & spread. High risk of rapid structural saturation, mold growth (critical in UAE climate), and electrical hazards. < 1 Hour Fire Incident (Post-Extinguishing) 1. Secure the area. 2. Document all untouched areas. High risk of evidence contamination. Soot, smoke, and water damage from suppression are crucial to capture for the claim. < 2 Hours Structural Damage (e.g., impact) 1. Evacuate & restrict access. 2. Document from a safe distance. Extreme safety risk. Immediate danger of progressive collapse or further structural failure. Immediate HVAC Failure (e.g., chiller leak) 1. Isolate power. 2. Document leak source & affected equipment. Risk of electrical faults, costly equipment damage, and significant business interruption (downtime). < 4 Hours Vandalism/Break-in 1. Do not touch anything. 2. Document the entire scene. Critical for both police reports and insurance claims. Scene preservation is paramount for liability assessment. < 2 Hours This table serves as a training tool to standardise your team's response, shifting their mindset from reactive panic to a structured protocol that protects your organisation's financial interests. Understanding the critical difference between a simple damage report and an insurance-ready claim file is foundational. It transforms a chaotic event into a managed process, ensuring a clear path from incident to resolution without incurring preventable financial loss. Why Insurers Mandate Documentation Before Repairs From an insurer's perspective, undertaking permanent repairs before a formal assessment is akin to destroying evidence. Loss adjusters are tasked with verifying the cause, scope, and liability associated with the damage, and this requires an unaltered scene. Without clear, time-stamped proof, it is difficult to distinguish a new incident from pre-existing wear and tear or poor maintenance—common exclusions in many commercial property policies. A well-intentioned but premature repair can be misinterpreted as an attempt to obscure the true nature of the incident, immediately raising red flags. Preserving the Chain of Evidence The damaged area constitutes critical evidence. Your photographic and written records create an unbroken "chain of custody" that validates what happened, where, and when. This documentation is the primary tool for successful claim settlement. The entire claims process is predicated on this initial evidence. It provides the loss adjuster with the necessary data to: Establish Causation: Was the damage from a sudden and unforeseen event (typically covered), or a slow leak resulting from deferred maintenance (often excluded)? Validate Scope of Work: Does the evidence support a full replacement of an asset, or merely a localised repair? Assess Third-Party Liability: Could a contractor, neighbouring tenant, or other third party be responsible for the loss? Insurers operate on verifiable data. Missing documentation creates ambiguity, and in the context of insurance, ambiguity leads to delays, disputes, or claim denials. Lessons from Recent UAE Weather Events The importance of the "document first" protocol was starkly highlighted during major weather events in the UAE. Following the unprecedented rainfall in April 2024, which generated estimated insured losses approaching US$850 million, many asset managers who initiated immediate clean-up and repairs without comprehensive documentation faced claim rejections. Insurers had no verifiable way to link the claimed damage directly to the insurable event. Data from the aftermath showed that properties with immediate, systematic digital documentation systems in place recovered their financial losses up to 40% more efficiently than those relying on manual processes. This event provided a clear lesson: in the UAE's commercial property market, documentation must precede action. Guidance for Procurement Teams: This risk mitigation strategy can be embedded directly into your service contracts. Mandate specific photo-documentation standards and response protocols within your Annual Maintenance Contracts (AMCs). This makes your service provider contractually obligated to preserve evidence before commencing work, shielding your organisation from the financial impact of a denied claim. To facilitate claim approval, it is

What Evidence Do Insurance Loss Adjusters Look For During Site Inspections?

When a loss adjuster steps onto a commercial property in the UAE, their objective is singular: to build a factual, evidence-based narrative of the incident. For property managers, facility leaders, and asset owners, understanding this process is not about confrontation; it's about providing the specific, verifiable data needed to validate a claim against policy terms. The adjuster's role is to connect three critical elements: the root cause of the incident, the quantifiable scope of the damage, and the mitigation actions taken by the policyholder to control the loss. The Adjuster's Mindset: Key Evidence Categories for Commercial Properties For decision-makers managing high-value assets in Dubai and the UAE, preparing for an adjuster's visit is a core risk management function. The adjuster acts as an impartial investigator, tasked with verifying the facts of the loss against the specific conditions and exclusions of the insurance policy. In the UAE's operational environment—characterised by high-density vertical assets and climate-driven MEP stress—an incident like a pipe burst or electrical failure can escalate into a multi-million dirham loss within minutes. The quality and structure of the initial evidence presented by the facility management team are therefore paramount. A well-prepared team can transform a complex loss scenario into a straightforward validation exercise for the adjuster. Core Areas of Evidentiary Focus An adjuster's site inspection is a structured process designed to gather evidence across four distinct pillars: Cause and Origin: Pinpointing the exact source of the loss. Was it a sudden and accidental failure of a pressurised pipe, a gradual leak from an HVAC condensate line, or a fault in an electrical busbar? The evidence must clearly point to the origin to confirm coverage under the policy. Proof of Pre-Loss Condition: Establishing the operational state of the asset before the incident. This is the primary defence against assertions of poor maintenance, wear and tear, or pre-existing defects, which are common grounds for claim reduction or denial. Loss Mitigation Efforts: Demonstrating immediate, reasonable, and documented actions taken to control the damage. This fulfills a key policy condition and shows responsible management of the insurer's potential exposure. Scope and Quantum of Damage: A detailed, itemised quantification of all damaged property and associated financial loss, forming the basis of the claim's value. The principles behind navigating home insurance claims share a similar logic, focusing on cause, effect, and mitigation, applicable across both residential and commercial asset classes. The loss adjuster’s primary function during a site inspection is to reconstruct the event timeline. They use physical evidence and operational documentation to answer three core questions: What failed? Why did it fail? What immediate actions were taken to limit the consequences? A facility manager's ability to provide clear, organised, and data-backed answers is the single most critical factor in achieving an efficient and fair claim settlement. Understanding the specific technical proof your insurer expects is a strategic advantage. The following framework outlines these evidence categories in a property management context. Core Evidence Categories for UAE Loss Adjusters This table outlines the essential evidence an adjuster seeks, its purpose, and its direct impact on your insurance claim's outcome. Evidence Category What Adjusters Scrutinize Impact on Claim Outcome Property Type Application Cause & Origin BMS logs, alarm data, CCTV footage, photos of the precise failure point (e.g., fractured pipe, arcing switchgear). High: Confirms the event is a covered peril under the policy terms. All (Commercial, Hospitality, Industrial, Retail) Pre-Loss Condition Annual Maintenance Contract (AMC) records, service reports, dated photos/videos of MEP rooms. High: Defends against policy exclusions related to negligence, wear and tear, or deferred maintenance. Commercial & Hospitality Mitigation Efforts Dispatch logs, timestamped photos of temporary fixes (e.g., water isolation, deployment of dehumidifiers), invoices for emergency services. Medium: Fulfills the policyholder's "duty to mitigate," preventing claim reduction on grounds of inaction. All Scope of Damage Itemised asset registers, independent contractor repair estimates, detailed photos/videos of all affected areas and contents. High: Forms the basis for the financial settlement ("quantum") of the loss. All Presenting this evidence proactively demonstrates operational competence and significantly accelerates the validation process, leading to a more predictable claim timeline. Proving Your Immediate and Effective First Response The initial 60-120 minute window following an incident is subject to the most intense scrutiny by an insurance adjuster. Your team's actions during this period provide a clear narrative: did the facility management team act responsibly and effectively to mitigate further loss? This is not a procedural formality; it is a core policy obligation that directly influences the final settlement amount. In a high-rise commercial tower or a large-scale hotel in Dubai, a single plumbing failure can cascade into a multi-floor, multi-million dirham event in under an hour. Insurers are acutely aware of this risk. Consequently, the evidence an adjuster seeks is heavily weighted toward the quality and timeliness of the initial response. They are looking for a clear, timestamped record proving that all reasonable measures were taken to contain the damage. Documenting Your Loss Mitigation Actions The objective of first-response documentation is to demonstrate control, compliance with internal protocols, and fulfillment of the policy's mitigation clause. The adjuster requires a sequential, undeniable record of your team's actions. Key evidence includes: Initial Discovery and Alert Logs: The precise timestamp of the initial alert (e.g., BMS alarm at 02:15, security report at 02:17), the source, and the individual who reported it. Emergency Call Records: A log of calls to on-call technical staff or third-party emergency contractors, including timestamps and personnel names. Technician Dispatch Records: System-generated proof of when a technician was assigned and, critically, their arrival time on site. This is a key performance indicator for responsiveness. System Isolation Confirmations: Photographic evidence of immediate safety actions, such as a closed water riser valve or an isolated electrical breaker, with the photo's metadata serving as a timestamp. This level of meticulous record-keeping confirms that actions were swift and decisive, meeting the professional standards expected in the UAE’s commercial property sector. The Power of Sequential Photographic Evidence Photographs are the most compelling form of evidence, but only

Why Proactive HVAC Maintenance Is Critical for Commercial Buildings in Dubai?

Heating, Ventilation, and Air Conditioning (HVAC) systems are among the most critical and cost-intensive assets in commercial buildings. In offices, retail spaces, hotels, healthcare facilities, and mixed-use developments, HVAC performance directly affects occupant comfort, energy consumption, indoor air quality, and business continuity. Despite this, HVAC maintenance is often approached reactively, with attention given only when cooling failures, complaints, or breakdowns occur. For commercial buildings in Dubai’s climate, this approach carries significant operational and financial risk. 1. The Role of HVAC Systems in Commercial Buildings HVAC systems regulate temperature, humidity, ventilation, and air filtration. They include chillers or split systems, air handling units (AHUs), fan coil units (FCUs), ductwork, controls, thermostats, and associated electrical and plumbing components. Any degradation in HVAC performance can impact occupant productivity, tenant satisfaction, and regulatory compliance. 2. Climate Stress and System Load in Dubai Dubai’s climate places continuous and heavy demand on HVAC systems for most of the year. Extended run hours, high ambient temperatures, dust, and humidity accelerate wear on coils, compressors, fans, and controls. Without proactive maintenance, minor inefficiencies can quickly escalate into major failures. 3. Energy Efficiency and Operating Cost Impact HVAC systems are typically the largest consumers of electricity in commercial buildings. Issues such as dirty coils, blocked filters, refrigerant imbalance, sensor drift, or poor airflow increase energy consumption while reducing cooling effectiveness. Routine inspection, cleaning, and calibration help maintain design efficiency and control energy costs. 4. Indoor Air Quality (IAQ) and Occupant Health Poorly maintained HVAC systems can contribute to indoor air quality issues, including dust accumulation, microbial growth, and inadequate ventilation. In commercial environments—particularly offices, clinics, and retail spaces—IAQ concerns can lead to occupant discomfort, health complaints, and reputational risk. Proactive maintenance supports clean air delivery and compliance with hygiene expectations. 5. Downtime, Complaints, and Business Disruption HVAC failures often result in immediate operational disruption, tenant complaints, or partial shutdown of affected areas. Reactive repairs typically involve longer downtime due to fault diagnosis, spare parts procurement, and emergency mobilization. Planned preventive maintenance reduces the likelihood and severity of such disruptions. 6. Asset Life, Capital Planning, and Risk Reduction Neglected HVAC systems experience accelerated component wear, leading to premature replacement and unplanned capital expenditure. Preventive maintenance extends equipment life, stabilizes performance, and supports informed capital planning. 7. Documentation, Compliance, and Insurance Considerations Maintenance records play an important role during audits, compliance checks, and insurance claims related to HVAC failures. Lack of documented maintenance may complicate claims or raise questions about reasonable care. Structured HVAC maintenance provides inspection logs, service records, and performance documentation. How Structured HVAC Maintenance Adds Value Engineering-led facility management companies such as SnapFixNow™ FMC deliver HVAC maintenance through planned inspections, performance monitoring, preventive servicing, and condition-based interventions. This approach supports reliability, energy efficiency, and long-term asset protection. More information on HVAC maintenance services is available at: Final Thought In Dubai’s operating environment, HVAC maintenance is not optional—it is a core business continuity and cost control function. For commercial buildings, proactive HVAC maintenance consistently delivers better comfort, efficiency, and risk management than reactive repair models.

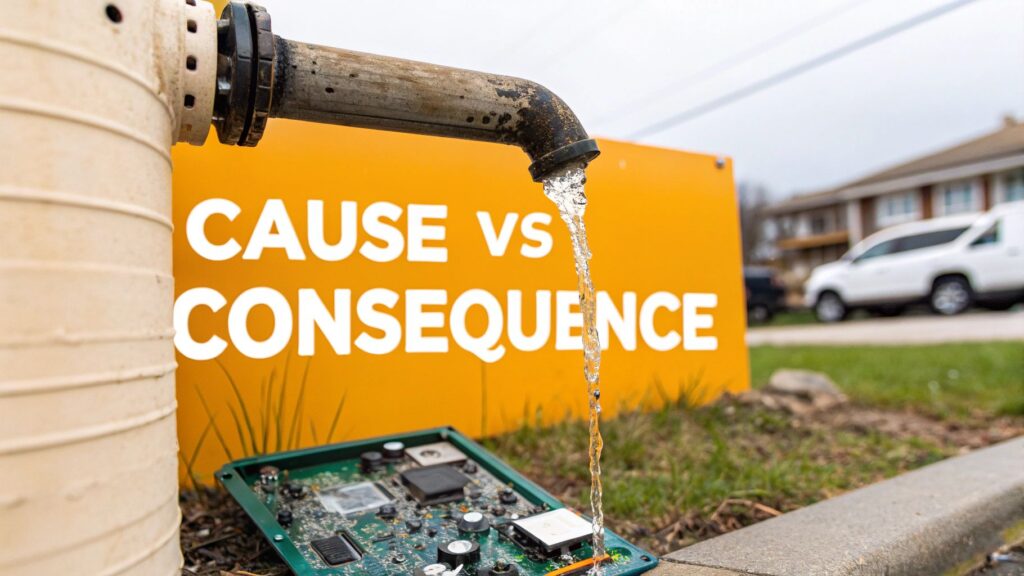

Water Leakage or Electrical Damage? How Insurers Assess Cause vs Consequence

For property and facility managers in Dubai and the UAE, a critical incident often raises a single, financially pivotal question: was the event triggered by water leakage or electrical damage? Insurers methodically separate the triggering event (the cause) from the resulting damage (the consequence). Understanding this distinction is fundamental to navigating the claims process and mitigating financial risk. A typical commercial property policy may cover the consequential damage from a burst pipe—such as ruined servers or flooring—but it will likely exclude the cost of repairing the pipe itself, especially if the failure resulted from gradual corrosion or inadequate maintenance. For asset owners and their operational teams, mastering this cause-and-effect assessment framework is the key to a successful claim submission. Understanding Cause vs. Consequence in Commercial Property Claims In the UAE's high-value property market, the financial impact of a claim is significant. For managers of commercial towers, hospitality assets, or large-scale residential communities, a poorly substantiated claim can lead to operational downtime and substantial, unbudgeted capital expenditure. Insurers and their appointed loss adjusters have one primary objective: to identify the single, dominant "proximate cause" that initiated the chain of events. This initial determination dictates which policy clauses are triggered, whether specific exclusions apply, and the ultimate settlement value. The facility or property manager's role is to provide clear, verifiable technical evidence that a covered peril was the proximate cause. The Insurer's Analytical Framework Insurers deconstruct damage into a sequence of events. An electrical short circuit may be the proximate cause, but the ensuing fire and the subsequent water damage from the building's sprinkler system are the consequences. While the fire and water damage are likely covered perils, the initial electrical fault may not be if it resulted from an excluded cause, such as gradual deterioration (wear and tear). A policyholder's ability to demonstrate a sudden, accidental, and unforeseen event as the proximate cause is paramount. Insurers are specifically looking to differentiate this from damage arising from wear and tear, faulty workmanship, or lack of preventive maintenance—all common policy exclusions. This distinction is especially critical in Dubai, where the climate—with its high humidity and temperature fluctuations—can accelerate material degradation. For example, ambient humidity can corrode electrical components over time, blurring the line between a sudden failure and a gradual one. An insurer will invariably request detailed maintenance records to determine if the failure was preventable through a diligent Annual Maintenance Contract (AMC). The matrix below illustrates how insurers typically analyse these incidents, providing a framework for facility managers to anticipate the investigation's focus. Insurer's Cause vs. Consequence Assessment Matrix This matrix provides a reference for how insurers categorize common water and electrical incidents, enabling facility managers to prepare for the technical scrutiny of a claim investigation. Incident Scenario Potential Proximate Cause (The Insured Peril) Resulting Damage (The Consequence) Primary Focus of Insurer's Investigation Chilled water pipe bursts, flooding an IT server room and shorting equipment. Sudden and accidental water discharge. Damage to servers, flooring, and electrical wiring. Verifying pipe condition and maintenance history (e.g., pressure tests, NDT reports) to rule out gradual corrosion or pre-existing leaks. Electrical fire in a DEWA room damages pumps, causing a loss of water pressure. Fire originating from an electrical fault. Fire and smoke damage to the room; consequential damage from pump failure. Forensic analysis of the electrical panel to pinpoint the exact point and reason for failure (e.g., surge vs. faulty component). AC unit condensate drain clogs and overflows, slowly seeping into walls. Gradual water ingress due to lack of maintenance. Mold growth, drywall degradation, and potential electrical faults in wall sockets. Reviewing AMC logs to confirm if drain lines were regularly cleaned; cause is often excluded as preventable. A power surge from the grid damages a building's main distribution panel. External electrical surge. Damage to the panel and connected equipment. Examining DEWA reports and building systems (BMS/SCADA data) for evidence of a surge event, differentiating it from an internal fault. The insurer's investigation will consistently revert to the root cause. As a facility manager, understanding their investigative path allows you to prepare the precise technical evidence required. Unpacking the Insurer's Investigation Process Reporting an incident of water leakage or electrical damage initiates a methodical investigation, not an automatic approval. For property and facility managers across the UAE, understanding this process is crucial for managing stakeholder expectations and preparing the necessary evidence to substantiate a claim. The insurer's objective is to trace the chain of events back to its origin. The process begins with the First Notification of Loss (FNOL). Upon reporting the damage, the insurer assigns a claim number and appoints a loss adjuster. These independent professionals act as the insurer's technical assessors on-site, tasked with evaluating the damage and determining the proximate cause. For high-value commercial claims, expect a site visit within 24 to 72 hours. During this initial assessment, the adjuster focuses on fact-gathering, mitigating further loss, and identifying immediate remediation needs. However, their primary function is to begin the root cause analysis. The Role of Technical Specialists and Evidence Review When the cause is not immediately apparent—a common scenario in complex MEP systems within commercial towers, industrial facilities, or hotels—loss adjusters engage third-party specialists. Forensic Engineers: These experts analyse material failures. For a burst pipe, they examine the ruptured section for evidence of corrosion, manufacturing defects, or external impact, differentiating between a gradual failure and a sudden event. MEP (Mechanical, Electrical, Plumbing) Specialists: For a suspected electrical fault, MEP consultants inspect panels, wiring, and equipment to identify the point of failure. Their report is critical for distinguishing an internal malfunction from an external event like a power surge. These specialists require access to a comprehensive suite of documents. Insurers scrutinise these records to establish a timeline and verify compliance. You can learn more about preparing the technical proof your insurer expects in our detailed guide. In claims assessment, the burden of proof rests with the policyholder. A well-organised digital file containing maintenance logs, AMC documentation, and incident reports not only expedites

Why Proactive MEP Maintenance Matters for Commercial Buildings in Dubai?

Mechanical, Electrical, and Plumbing (MEP) systems form the backbone of any commercial building. In offices, retail spaces, hotels, and mixed-use developments, MEP systems directly impact safety, comfort, uptime, and operating costs. Despite this, many building owners underestimate the importance of structured MEP maintenance until failures begin to disrupt operations. Understanding why proactive MEP maintenance matters is critical for long-term asset performance and risk control. 1. What MEP Systems Cover in Commercial Buildings MEP systems typically include HVAC equipment, electrical distribution boards, lighting systems, power backup, plumbing networks, pumps, drainage, and control systems. Failures in any of these areas can affect not only comfort, but also life safety, regulatory compliance, and business continuity. 2. The Hidden Cost of Neglected MEP Systems MEP failures rarely occur suddenly. They often develop due to undetected wear, imbalance, improper calibration, or deferred servicing. Without preventive maintenance, small inefficiencies escalate into breakdowns, emergency repairs, and unplanned capital expenditure. 3. Impact on Energy Efficiency and Operating Costs Poorly maintained HVAC and electrical systems consume more energy to deliver the same output. Issues such as clogged coils, imbalanced airflows, loose electrical connections, and leaking valves increase utility costs and shorten equipment life. Proactive maintenance helps maintain system efficiency and control operating expenses. 4. Risk, Safety, and Compliance Considerations MEP systems are closely linked to fire safety, electrical safety, water hygiene, and indoor air quality. Neglected maintenance can lead to non-compliance findings, safety incidents, and increased liability exposure. Routine inspections and documented servicing support regulatory and insurance requirements. 5. Downtime and Business Continuity In commercial environments, MEP failures often result in operational downtime, tenant complaints, or business interruption. Reactive repairs typically involve longer restoration times due to fault tracing, part sourcing, and emergency mobilization. Planned maintenance reduces the likelihood and impact of disruptive failures. 6. Documentation and Insurance Implications Insurance claims related to MEP failures often require proof of reasonable maintenance practices. Lack of maintenance records can complicate claims or lead to partial settlement. Structured MEP maintenance provides inspection logs, service records, and technical documentation that support claim credibility. How Structured MEP Maintenance Adds Value Engineering-led facility management companies such as SnapFixNow™ FMC approach MEP maintenance through planned inspections, performance monitoring, and preventive servicing aligned with asset criticality. This approach supports reliability, cost control, and long-term asset protection. More information on MEP maintenance services is available at: Final Thought MEP maintenance is not simply a technical task,it is a risk management and cost control function. For commercial buildings, proactive MEP maintenance consistently delivers better reliability, compliance, and financial outcomes than reactive repair models.