For property and facility managers in Dubai and the UAE, a critical incident often raises a single, financially pivotal question: was the event triggered by water leakage or electrical damage? Insurers methodically separate the triggering event (the cause) from the resulting damage (the consequence). Understanding this distinction is fundamental to navigating the claims process and mitigating financial risk.

A typical commercial property policy may cover the consequential damage from a burst pipe—such as ruined servers or flooring—but it will likely exclude the cost of repairing the pipe itself, especially if the failure resulted from gradual corrosion or inadequate maintenance. For asset owners and their operational teams, mastering this cause-and-effect assessment framework is the key to a successful claim submission.

Understanding Cause vs. Consequence in Commercial Property Claims

In the UAE's high-value property market, the financial impact of a claim is significant. For managers of commercial towers, hospitality assets, or large-scale residential communities, a poorly substantiated claim can lead to operational downtime and substantial, unbudgeted capital expenditure. Insurers and their appointed loss adjusters have one primary objective: to identify the single, dominant "proximate cause" that initiated the chain of events.

This initial determination dictates which policy clauses are triggered, whether specific exclusions apply, and the ultimate settlement value. The facility or property manager's role is to provide clear, verifiable technical evidence that a covered peril was the proximate cause.

The Insurer's Analytical Framework

Insurers deconstruct damage into a sequence of events. An electrical short circuit may be the proximate cause, but the ensuing fire and the subsequent water damage from the building's sprinkler system are the consequences. While the fire and water damage are likely covered perils, the initial electrical fault may not be if it resulted from an excluded cause, such as gradual deterioration (wear and tear).

A policyholder's ability to demonstrate a sudden, accidental, and unforeseen event as the proximate cause is paramount. Insurers are specifically looking to differentiate this from damage arising from wear and tear, faulty workmanship, or lack of preventive maintenance—all common policy exclusions.

This distinction is especially critical in Dubai, where the climate—with its high humidity and temperature fluctuations—can accelerate material degradation. For example, ambient humidity can corrode electrical components over time, blurring the line between a sudden failure and a gradual one. An insurer will invariably request detailed maintenance records to determine if the failure was preventable through a diligent Annual Maintenance Contract (AMC).

The matrix below illustrates how insurers typically analyse these incidents, providing a framework for facility managers to anticipate the investigation's focus.

Insurer's Cause vs. Consequence Assessment Matrix

This matrix provides a reference for how insurers categorize common water and electrical incidents, enabling facility managers to prepare for the technical scrutiny of a claim investigation.

| Incident Scenario | Potential Proximate Cause (The Insured Peril) | Resulting Damage (The Consequence) | Primary Focus of Insurer's Investigation |

|---|---|---|---|

| Chilled water pipe bursts, flooding an IT server room and shorting equipment. | Sudden and accidental water discharge. | Damage to servers, flooring, and electrical wiring. | Verifying pipe condition and maintenance history (e.g., pressure tests, NDT reports) to rule out gradual corrosion or pre-existing leaks. |

| Electrical fire in a DEWA room damages pumps, causing a loss of water pressure. | Fire originating from an electrical fault. | Fire and smoke damage to the room; consequential damage from pump failure. | Forensic analysis of the electrical panel to pinpoint the exact point and reason for failure (e.g., surge vs. faulty component). |

| AC unit condensate drain clogs and overflows, slowly seeping into walls. | Gradual water ingress due to lack of maintenance. | Mold growth, drywall degradation, and potential electrical faults in wall sockets. | Reviewing AMC logs to confirm if drain lines were regularly cleaned; cause is often excluded as preventable. |

| A power surge from the grid damages a building's main distribution panel. | External electrical surge. | Damage to the panel and connected equipment. | Examining DEWA reports and building systems (BMS/SCADA data) for evidence of a surge event, differentiating it from an internal fault. |

The insurer's investigation will consistently revert to the root cause. As a facility manager, understanding their investigative path allows you to prepare the precise technical evidence required.

Unpacking the Insurer's Investigation Process

Reporting an incident of water leakage or electrical damage initiates a methodical investigation, not an automatic approval. For property and facility managers across the UAE, understanding this process is crucial for managing stakeholder expectations and preparing the necessary evidence to substantiate a claim. The insurer's objective is to trace the chain of events back to its origin.

The process begins with the First Notification of Loss (FNOL). Upon reporting the damage, the insurer assigns a claim number and appoints a loss adjuster. These independent professionals act as the insurer's technical assessors on-site, tasked with evaluating the damage and determining the proximate cause. For high-value commercial claims, expect a site visit within 24 to 72 hours.

During this initial assessment, the adjuster focuses on fact-gathering, mitigating further loss, and identifying immediate remediation needs. However, their primary function is to begin the root cause analysis.

The Role of Technical Specialists and Evidence Review

When the cause is not immediately apparent—a common scenario in complex MEP systems within commercial towers, industrial facilities, or hotels—loss adjusters engage third-party specialists.

- Forensic Engineers: These experts analyse material failures. For a burst pipe, they examine the ruptured section for evidence of corrosion, manufacturing defects, or external impact, differentiating between a gradual failure and a sudden event.

- MEP (Mechanical, Electrical, Plumbing) Specialists: For a suspected electrical fault, MEP consultants inspect panels, wiring, and equipment to identify the point of failure. Their report is critical for distinguishing an internal malfunction from an external event like a power surge.

These specialists require access to a comprehensive suite of documents. Insurers scrutinise these records to establish a timeline and verify compliance. You can learn more about preparing the technical proof your insurer expects in our detailed guide.

In claims assessment, the burden of proof rests with the policyholder. A well-organised digital file containing maintenance logs, AMC documentation, and incident reports not only expedites the process but also lends critical credibility to the claim.

Regulatory Compliance and Final Assessment

The adjuster's investigation is also framed by local regulations. They will verify if damaged systems were installed and maintained in accordance with Dubai Municipality building codes and DEWA (Dubai Electricity and Water Authority) standards. Non-compliance can be flagged as negligence, potentially jeopardising the claim.

The unprecedented April 2024 floods in the UAE, which resulted in insured losses estimated between $2.15 billion and $2.95 billion, offer a case study. Loss adjusters were tasked with meticulously separating cause from consequence. Was the floodwater the primary peril, or did pre-existing issues like inadequate waterproofing or faulty plumbing exacerbate the electrical damage?

The process concludes with the loss adjuster's final report. This document consolidates all findings: photographic evidence, specialist reports, witness statements, and a policy review. It culminates in their professional opinion on the proximate cause, which directly informs the insurer’s settlement decision.

When it comes to complex property damage, the line between water leakage and electrical failure can be blurry. Insurers in the UAE are adept at untangling these interconnected events to pinpoint the legally-defined proximate cause. Understanding their methodology is key to building a successful claim.

The entire investigation reconstructs the sequence of events. Did a mechanical failure (e.g., burst pipe) occur first, leading to an electrical fault (e.g., short circuit)? Or did an electrical event (e.g., power surge) cause a mechanical breakdown (e.g., pump seizure), which then resulted in a leak? The answer determines the claim's direction.

Let’s analyse two common scenarios in Dubai’s high-rise assets. This comparison highlights how an insurer’s focus shifts based on the initial trigger.

Scenario A: The Water-Initiated Pathway

A chilled water pipe within a tower's HVAC system ruptures above a critical electrical room. The subsequent water ingress floods a main distribution board, causing a major short circuit.

Here, the proximate cause is "sudden and accidental discharge of water." The electrical damage is the consequence. The insurer's investigation will focus on the building's plumbing and mechanical systems.

The loss adjuster will investigate:

- Maintenance History: Were regular pressure tests and visual inspections of chilled water lines conducted as per the Annual Maintenance Contract (AMC)? They will demand access to maintenance logs.

- Material Condition: Did the pipe fail due to gradual corrosion, a known defect, or an unforeseen event? Forensic engineers may be engaged to analyse the ruptured section.

- System Age & Lifespan: Was the pipe nearing its expected service life (often 15-25 years for certain materials in the region's climate)? A failure in an aged, poorly maintained system can be attributed to wear and tear.

The burden is on the policyholder to demonstrate that the pipe failure was a sudden, unforeseeable event, not a predictable failure resulting from neglected maintenance.

Scenario B: The Electrical-Initiated Pathway

A major power surge from the grid impacts the building. The surge damages the control panel for a water booster pump, causing it to malfunction. The pump over-pressurises the system, leading to a pipe rupture and a significant leak.

In this case, the proximate cause is "electrical surge" or "equipment breakdown" from an external event. The water leak and all subsequent damage are the consequences.

The investigation shifts entirely to the electrical infrastructure:

- Surge Protection: Does the building have appropriate surge protection devices (SPDs) at main distribution boards, as per DEWA guidelines?

- External Evidence: Is there a record of the surge? Investigators will seek DEWA reports or data logs from the Building Management System (BMS) showing a voltage anomaly.

- Equipment Failure Analysis: An MEP specialist will examine the pump's control panel for evidence of electrical damage—such as arc flashes or burnt circuits—that predates the water damage.

For facility managers, this distinction is critical. In Scenario A, plumbing and HVAC maintenance records are paramount. In Scenario B, electrical system schematics, maintenance logs, and evidence of compliant surge protection are the key determinants of success.

Comparative Analysis: Water-Initiated vs. Electrical-Initiated Damage

This framework breaks down the two pathways to illustrate the insurer's analytical process for determining which peril—water leakage or electrical damage—was the true proximate cause.

| Assessment Criterion | Scenario A: Burst Pipe Causes Electrical Short | Scenario B: Power Surge Damages Pump Causing Leak |

|---|---|---|

| Identified Proximate Cause | Sudden discharge of water from a plumbing or HVAC system. | Electrical surge or sudden electrical equipment failure. |

| Primary Evidence Required | AMC logs for plumbing/HVAC, pipe material analysis, pressure test records, BMS alerts for pressure drops. | DEWA reports, BMS data showing voltage spikes, forensic report on the pump's control panel, SPD maintenance records. |

| Key Policy Clause Triggered | Water Damage / Escape of Water Peril. | Electrical Damage or Machinery Breakdown Peril (if endorsed). |

| Potential Policy Exclusions | Gradual damage (slow leak), corrosion, wear and tear, lack of preventive maintenance on the pipe. | Lack of surge protection, faulty installation of electrical equipment, pre-existing electrical faults. |

| Probable Coverage Outcome | Cost to repair/replace damaged electrical board is likely covered. Cost to repair the burst pipe itself may be excluded. | Cost of repairing/replacing the pump and resulting water damage is likely covered. Cost of installing new SPDs is excluded. |

A successful claim depends on presenting a clear, evidence-backed narrative that directly links the damage to a covered peril as the proximate cause. By anticipating the insurer's line of inquiry, you can prepare the precise documentation needed to substantiate your case and achieve a fair and timely resolution.

Mastering Documentation and Evidence Management

The quality of documentation is the single most important factor in claim management. The initial hours following a water leak or electrical failure are critical. The evidence collected—or omitted—can determine the outcome of your claim. For facility managers, a methodical approach is a non-negotiable operational discipline.

This requires more than informal photographs. It involves a systematic process: securing the scene, generating detailed incident reports with precise timestamps, and maintaining a verifiable archive of all maintenance activities. In the UAE's high-value commercial, hospitality, and retail sectors, a claim lacking robust evidence is a direct route to financial loss.

The Immediate Response Checklist

Upon incident discovery, on-site teams must execute a pre-defined protocol. The dual objectives are ensuring safety and preserving evidence. A disorganized response can compromise both, leading to further damage and a weakened insurance claim.

An effective on-site team checklist includes:

- Ensure Scene Safety: Isolate the area before any other action. De-energise electrical breakers or close main water valves to mitigate ongoing damage. The safety of occupants and staff is the first priority.

- Initial Photographic and Video Evidence: Document the scene extensively before any cleanup or alteration. Capture wide-angle shots to establish context and close-ups of the suspected failure point (e.g., the burst pipe, the damaged electrical panel). A video walkthrough provides an invaluable record of the damage's full extent.

- Create a Detailed Incident Report: This formal document must include the exact time of discovery, the reporting person, immediate actions taken, and an initial damage assessment. Ambiguous reports are ineffective; precision is key.

- Preserve Key Components: If a pipe, fitting, or electrical component has failed, do not discard it. The insurer's forensic engineer will require this physical evidence for analysis. Bag, tag, and secure the component for inspection.

Building an Irrefutable Evidence File

While immediate response is vital, the claim's strength is built on historical proof. Loss adjusters scrutinise maintenance records to rule out common exclusions like wear and tear or neglect. Modern facility management technologies are indispensable here.

Digital work order systems and a Computerised Maintenance Management System (CMMS) create a time-stamped, unalterable audit trail of all planned and reactive maintenance. This data provides objective proof of due diligence.

An insurer's investigation is fundamentally an audit of your operational procedures. A claim file supported by consistent, dated maintenance logs from a digital platform is exponentially more credible than one relying on paper records and memory.

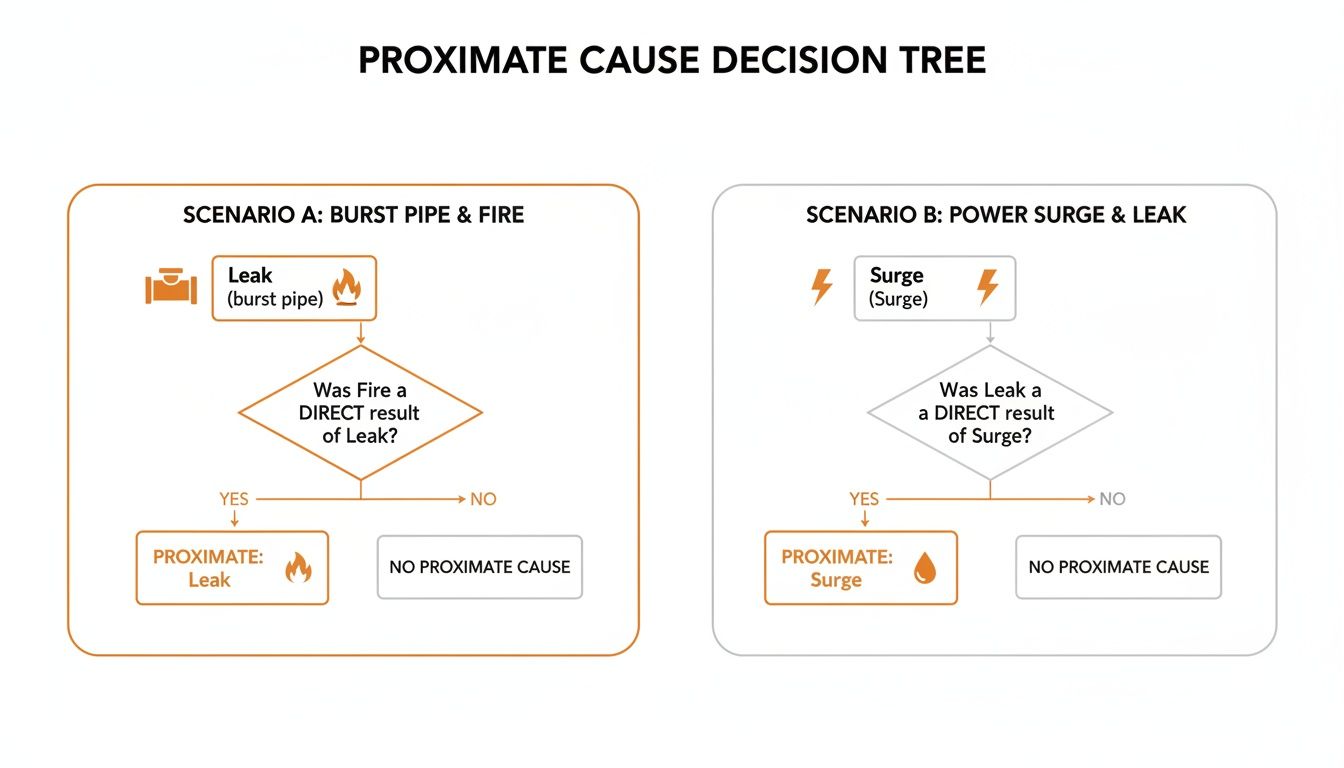

This decision tree illustrates an insurer's logic in tracing the proximate cause. The initial event dictates the entire investigative path.

As the diagram shows, two distinct pathways exist. Whether the trigger was a leak or a power surge determines the investigation's focus and the evidence required. For a comprehensive look at structuring this information, you can learn more about the difference between a damage report and an insurance-ready claim file in our specialised guide.

This disciplined approach applies to all major property claims. For example, a structured guide like a what to do after a house fire checklist demonstrates the same need for methodical documentation in other catastrophic events. A structured and diligent evidence management process protects the asset and streamlines the claims journey.

Navigating Critical Policy Exclusions and Endorsements

The success or failure of a claim is often determined by the policy's fine print. For facility and asset managers in the UAE, understanding what a policy explicitly excludes is as critical as knowing what it covers. Insurers use these clauses to manage their risk exposure; if their investigation links the proximate cause to an excluded event, the claim will be denied.

A standard property policy is designed to cover sudden and unforeseen events, not to function as a maintenance contract. It will therefore almost invariably exclude damage that occurs gradually or results from poor upkeep. The intensity of an insurer's investigation into a water leak or electrical fault stems directly from their need to check if the cause aligns with a policy exclusion.

Common Exclusions in UAE Property Policies

While policy wordings vary, several standard exclusions consistently appear in claims involving water and electricity. A thorough understanding of these is essential for risk management and for challenging claim rejections.

Common exclusions include:

- Gradual Damage: This is a primary exclusion. Damage from a slow-leaking pipe, moisture ingress from failed waterproofing, or the gradual degradation of electrical insulation is typically not covered.

- Wear and Tear: Assets have a finite operational lifespan. If a pump fails or a pipe bursts simply because it has reached the end of its service life, the insurer will exclude the replacement cost, arguing the failure was inevitable, not accidental.

- Faulty Workmanship or Design: If an electrical fire is traced to improper installation, or a major leak is the result of a design flaw in the plumbing system, the policy will not respond. Liability rests with the contractor or designer, not the insurer.

- Lack of Maintenance: This is a frequently cited clause. If maintenance logs show that scheduled servicing for an HVAC unit that caused a flood was missed, the insurer has grounds to deny the claim based on negligence.

An insurer's primary defence against a claim is often rooted in proving the proximate cause was an excluded event. For example, they may accept that a fire (a covered peril) occurred, but if they prove the fire was caused by aged, unmaintained wiring (wear and tear), the claim can be denied.

Enhancing Coverage with Policy Endorsements

A standard policy can be augmented with endorsements—amendments that add coverage for specific risks that would otherwise be excluded. For properties in the UAE, which face unique environmental and operational risks, carefully selected endorsements are a critical component of a robust risk management strategy.

Following the recent major floods, where insured property losses reached as high as $2.3 billion, the UAE insurance market has been significantly impacted. This has led to property premium increases of approximately 17%. Consequently, facility managers are now scrutinising policy terms more closely and investing in preventive AMCs to manage risks and costs. For context, see this analysis of the UAE's insurance market resilience. In such scenarios, understanding the specifics of how to file a flood insurance claim becomes essential.

Key endorsements to consider include:

- Flood and Storm Damage: Many basic policies exclude damage from natural floods or severe storms. In a region prone to sudden, intense rainfall, this endorsement is non-negotiable for commercial and residential assets.

- Machinery Breakdown: This covers the sudden and accidental breakdown of critical equipment—such as HVAC chillers, elevators, and water pumps—which a standard property policy may not cover.

- Business Interruption: If a covered event like a fire or major leak forces a hotel or commercial building to cease operations, this endorsement covers the resulting loss of income.

By strategically reviewing exclusions and adding appropriate endorsements, you can transform a generic insurance policy into a tailored risk management tool aligned with your property’s specific operational realities.

A Framework for Speeding Up Your Claim

A reactive approach is insufficient when managing a complex property insurance claim for water leakage or electrical damage. A structured, proactive methodology can significantly reduce delays and strengthen your negotiating position, converting a chaotic event into a manageable process.

For property and facility managers in Dubai, the objective is to submit a claim that is not merely complete but logically sound and easy to assess. This facilitates the loss adjuster's validation process and minimises the delays common in complex settlements.

Phase 1: The First Two Hours – Incident Response and Control

The initial 120 minutes post-incident are critical for safety and evidence preservation. The goal is to control the situation without contaminating the scene that the insurer’s investigator must analyse.

- Isolate and Secure: The immediate action is to de-energise electrical breakers or shut main water valves. A target response time of under 15 minutes from notification is a key performance indicator (KPI) for minimising consequential damage.

- Initial Documentation: Before any remediation begins, conduct extensive photographic and video documentation. This raw, timestamped visual data is the most compelling evidence in the initial stages.

- Formal Notification: Submit the First Notification of Loss (FNOL) to your insurer and broker within the first few hours. The notification should be factual and concise, avoiding speculation on the cause.

Phase 2: The Next 24-72 Hours – Coordinating with the Loss Adjuster

The engagement with the loss adjuster sets the tone for the entire claim process. The objective is to facilitate their investigation while presenting the documented facts clearly.

Be prepared to provide immediate access to all relevant maintenance records, including Annual Maintenance Contracts (AMCs), recent work orders, and BMS data logs. A well-organised digital file demonstrates professionalism and transparency.

An adjuster’s primary function is to identify the proximate cause. Your role is to guide them to the correct conclusion with objective, verifiable evidence. A collaborative, well-prepared approach is more effective than an adversarial one.

Phase 3: The First 7 Days – Building Your Comprehensive Claim Package

This phase involves consolidating all information into a single, organised submission. This package is your formal argument and should leave no room for ambiguity. It is also prudent to understand common pitfalls; learn more by reviewing why property insurance claims get delayed or rejected in Dubai.

Your submission package must include:

- A detailed incident report with a clear timeline.

- All photographic and video evidence.

- Copies of relevant AMCs and service reports.

- Repair quotations from qualified, vendor-neutral contractors.

- Statements from any staff or tenants who witnessed the event.

By following this framework, you shift from being a passive participant to an active manager of the claims process. This structured approach accelerates timelines, builds credibility, and ensures a fair outcome for your water leakage or electrical damage claim.

Frequently Asked Questions

Navigating the complexities of water and electrical damage claims raises common questions for facility managers in the UAE. Here are clear answers to the most frequent inquiries.

How Long Does a Complex Insurance Claim Investigation Take in Dubai?

For a complex claim involving both significant water and electrical damage, the investigation process typically ranges from four to twelve weeks. The timeline is influenced by several factors: the loss adjuster's availability, the need for third-party forensic reports (which can take 2-4 weeks alone), the quality and completeness of your documentation, and the level of cooperation between all parties.

Major city-wide events, such as severe storms, can significantly extend these timelines due to a surge in claims volume across the market.

Is a Report from Our In-House Maintenance Team Considered Valid Evidence?

Yes, an in-house report is a crucial piece of initial evidence, provided it is detailed, objective, and contemporaneous with the event. However, for claims exceeding a certain threshold (often around AED 250,000), the insurer will invariably appoint their own independent loss adjuster to conduct a separate assessment.

Your team’s report, supported by photographic evidence and digital maintenance logs, establishes a strong evidentiary foundation and demonstrates due diligence, which can expedite the validation process.

The credibility of an in-house report is significantly enhanced when generated by a digital CMMS. The system provides unalterable timestamps and a clear audit trail of maintenance activities, creating an objective record that is difficult to dispute.

What Is the Most Common Reason for Claim Denial in These Cases?

The most frequent reason for claim denial is the insurer attributing the proximate cause to a specific policy exclusion. The most common exclusions cited are gradual damage (e.g., from slow, undetected leaks), lack of preventive maintenance, or wear and tear.

For example, if an electrical fire is traced to aged wiring that was not maintained in line with documented standards, the claim may be rejected under a 'wear and tear' exclusion, even though fire itself is a covered peril. This underscores the critical importance of proving the damage resulted from a sudden and accidental event.

At SnapFixNow, we understand the critical role of robust documentation and rapid response in claim substantiation. Our team provides detailed technical reports and support for facility managers, ensuring you have the verifiable evidence required to navigate the insurance claims process for a fair and efficient resolution. Learn more about our specialised facility management services.