Filing a successful property damage claim in Dubai is not about luck; it is a structured process demanding precision from the outset. For property managers, facility managers, and asset owners, executing this process correctly protects asset value and ensures business continuity, especially when mitigating the region's unique climate-related risks. The methodology is rooted in three core disciplines: immediate response, meticulous documentation, and professional communication with the insurer.

Navigating Property Damage Claims in the UAE

When a pipe bursts in a commercial tower or a storm damages a hospitality asset, it triggers a critical business process, not just an operational headache. The objective for facility managers, asset owners, and procurement teams in Dubai is to restore the asset to its pre-loss condition with minimal financial and operational disruption. A fair and timely settlement hinges on a systematic approach that demonstrates due diligence from the moment the incident is discovered.

The commercial and regulatory environment in the UAE demands a high standard of preparation. Insurers operate in a competitive market and apply rigorous scrutiny to claims—especially large or complex ones involving commercial, hospitality, or industrial assets. A disorganised or poorly documented submission is a direct pathway to delays, disputes, and potential rejection, which directly impacts cash flow and operational stability.

The Financial Stakes of a Well-Prepared Claim

The financial impact of property damage extends beyond the immediate repair bill. Business interruption costs can be equally significant, a reality underscored by recent climate events.

In the wake of unprecedented heavy rainfall, UAE insurers faced estimated losses between $1.5 billion and $2.5 billion (Dh5.5 billion to Dh9.175 billion), predominantly from property damage claims. Post-event analysis shows that insurers are now rigorously examining policy fine print. Claims are being scrutinised for strict adherence to terms—deductibles, sub-limits, and exclusions, with a particular focus on maintenance logs. This has already led to a quantifiable increase in legal disputes. You can read more about the rise in UAE insurance claims on Khaleej Times.

This environment makes a proactive, evidence-based strategy essential. A successful claim is one where the submission is so clear and comprehensive that it pre-emptively answers the loss adjuster's questions, leaving no room for ambiguity. To align with industry trends, it is beneficial to have an understanding of automated claims processing to appreciate how insurers are leveraging technology to evaluate submissions.

A successful property damage insurance claim is built on a foundation of irrefutable evidence. Your goal is to present a narrative supported by timestamped data, expert analysis, and clear communication, effectively guiding the loss adjuster to the correct and fair conclusion without any friction.

The following sections provide a detailed, step-by-step guide designed for B2B stakeholders. We will cover every critical action, from the immediate incident response through to coordinating post-settlement repairs, enabling you to manage the entire claim lifecycle with confidence. This framework will help you convert a potential crisis into a manageable recovery process.

Your Immediate Response and Documentation Protocol

The first 72 hours are critical. When property damage occurs, actions taken within this initial window can determine the success of your entire insurance claim. For facility and property managers in Dubai, this is the period to shift from crisis management to a controlled, evidence-gathering operation—rapidly.

The priority is not to assign blame or calculate final costs. The mission is preservation: preserving the asset from further deterioration (e.g., mould ingress following water damage) and preserving all evidence required for a fair settlement. This requires a clear, immediate protocol that on-site teams can execute without hesitation.

Mobilising Your Immediate Response Team

Upon notification of an incident, your priorities are safety and stabilisation. This involves more than a simple call to a maintenance crew; it is a coordinated effort to secure the site and mitigate ongoing damage.

Your protocol should initiate several concurrent actions:

- Secure the Site: Immediately restrict access to the damaged area. This is a non-negotiable safety measure, particularly after a fire, structural failure, or major electrical fault, and it preserves the scene for investigation.

- Mitigate the Damage: Authorise immediate, essential actions to prevent further loss. This includes engaging specialists for water extraction, deploying industrial dehumidifiers, or boarding up compromised windows. These are not permanent repairs but essential first-aid measures.

- Issue First Notice of Loss (FNOL): Contact your insurance broker or the insurer’s claims department in writing. This initial notification does not require extensive detail but officially starts the claim timeline. An email with the date, time, location, and a brief incident description is sufficient.

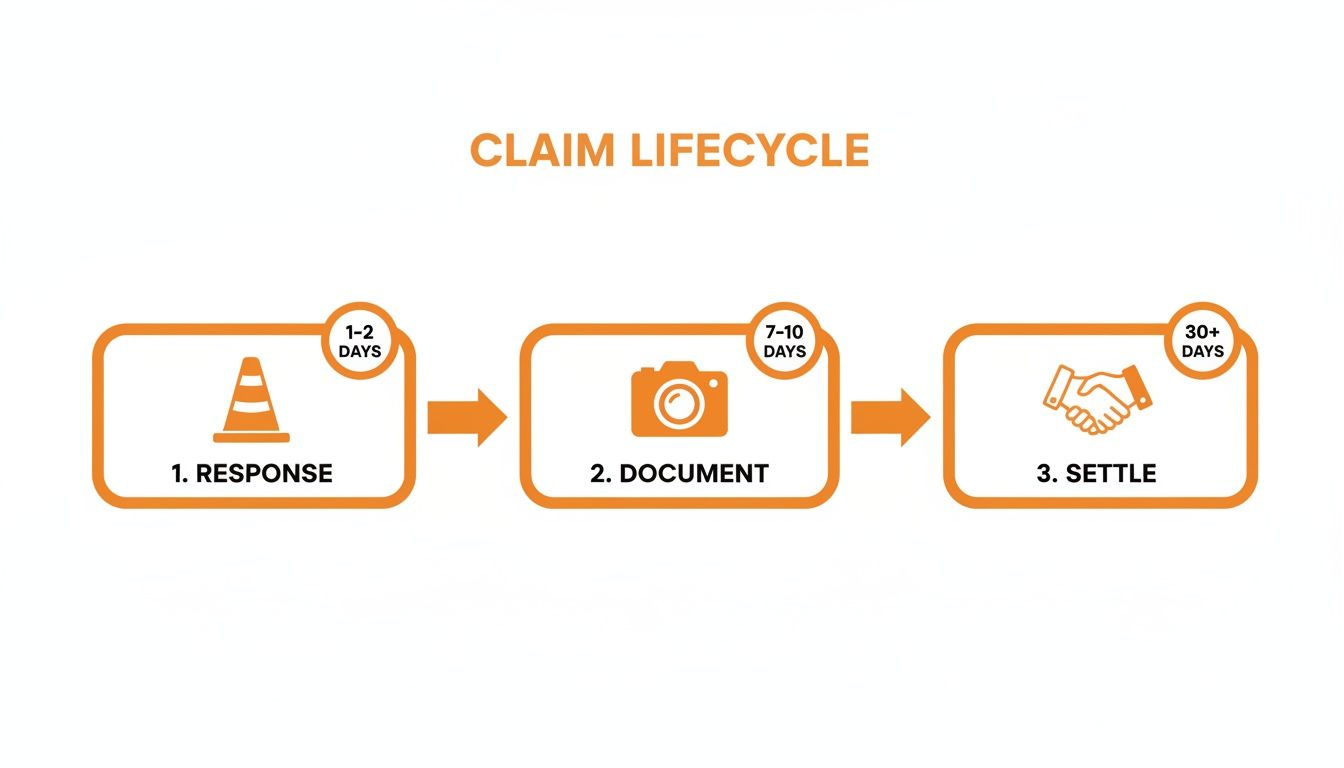

This timeline illustrates the claim lifecycle, highlighting the critical importance of the initial response and documentation phases.

As shown, the diligence applied at the start directly influences the efficiency of the subsequent stages.

The Gold Standard for Evidence Collection

Insurers in the UAE expect robust, verifiable proof. Insufficient evidence, such as a few low-resolution photos and a vague description, will not suffice. Your documentation must present a clear, chronological narrative of the damage and your response. Modern facility management platforms like SnapFixNow, which utilize photo-based work orders, are invaluable in creating a timestamped, auditable trail automatically.

Your evidence-gathering checklist should include:

- Comprehensive Photography: Capture hundreds of high-resolution images. Start with wide shots for context and then zoom in on specific damage points. Crucially, photograph the source of the damage—the burst pipe, the faulty electrical panel—before any mitigation work begins.

- Video Walk-through: A continuous 360-degree video of all affected areas provides an unfiltered view of the scene. Narrate the video as you record, pointing out key details such as the extent of water ingress or specific structural issues.

- Detailed Action Log: Maintain a written log of every action taken and every communication. Note the person spoken to, the date and time, and the key points discussed. This log becomes a critical reference during discussions with the loss adjuster.

An insurer's loss adjuster is trained to identify weaknesses in a claim. A meticulously documented file, containing timestamped photos and detailed logs of mitigation efforts, answers their questions proactively. It demonstrates professional diligence and can significantly accelerate the approval process.

Ultimately, the quality of your initial evidence is a primary determinant in how to prepare a successful property damage insurance claim in Dubai. The effort invested in these first days directly correlates with the speed and fairness of your final settlement, transforming a potential disaster into a manageable process.

Assembling Your Comprehensive Claim Dossier

Once the situation is stabilised, your focus must shift to compiling a robust claim dossier. This is not merely a collection of documents; it is the structured, evidence-based argument that underpins your settlement request. For asset managers and engineering leaders in Dubai, the quality of this submission is directly linked to the speed and success of the claim outcome.

The dossier serves as the single source of truth for the incident. A loss adjuster's function is to verify facts, and a well-organised file facilitates their work, reducing friction and the back-and-forth communications that extend claim durations.

Core Components of a Defensible Dossier

Every claim dossier must present a clear, chronological narrative. Each component serves a specific function, from proving coverage to detailing the full extent of the loss.

Your non-negotiable checklist should include:

- The Full Insurance Policy Document: This includes the policy schedule and all endorsements. It is the foundational document an adjuster will review to establish the terms of coverage.

- Initial Incident Report: Your internal record is vital. It should detail the exact date, time, and circumstances of the damage, along with the immediate mitigation actions taken.

- Official Reports (When Applicable): For major events such as fire, significant electrical faults, or vandalism, a Dubai Police report is typically mandatory. For certain utility-related incidents, a DEWA report may be required.

- Comprehensive Photographic and Video Evidence: This forms the visual backbone of your claim, showing the damage before, during, and after initial mitigation work.

A crucial part of a strong dossier is a detailed inventory of damaged assets. Excellent guidance is available on creating a home inventory for insurance. While the guide is residential-focused, its principles of detailed cataloguing are directly applicable to commercial assets.

The Role of Third-Party Technical Assessments

This is a critical differentiator for complex claims. While internal reports are important, independent assessments from certified engineers or specialists add a layer of credibility that is difficult for insurers to dispute. These reports elevate a claim from a simple request to a technically validated case.

For instance, following a major water leak in a commercial tower, a detailed MEP (Mechanical, Electrical, and Plumbing) assessment is essential. It will not only quantify damage to pumps, chillers, and electrical panels but also provide a root cause analysis—a key piece of information for the insurer. Having the right technical proof for your insurance claim can be decisive.

The required level of detail varies by asset type:

- Hospitality: A claim for a hotel often involves a significant business interruption component. This requires not just repair quotes but also financial records demonstrating lost revenue, supported by historical occupancy rate data.

- Industrial: Damage to specialised machinery necessitates an assessment from a qualified equipment specialist to determine the feasibility and cost-effectiveness of repair versus replacement.

- Retail: In a retail environment, the claim must clearly differentiate between damage to the building's structure (landlord's policy) and damage to stock or fit-outs (tenant's policy), each requiring distinct documentation.

The quality of your submission directly impacts the outcome.

Claim Submission Quality Comparison Framework

| Claim Element | Weak Submission (High Risk of Delay or Denial) | Strong Submission (Optimized for Successful Settlement) |

|---|---|---|

| Initial Report | Vague, handwritten notes with missing times or details. | A typed, dated report with a clear timeline of events and immediate actions taken. |

| Photographic Evidence | A few blurry, poorly lit phone photos of the final damage. | Dozens of high-resolution, dated photos/videos from multiple angles, showing context and scale, including pre-mitigation shots. |

| Damage Assessment | A single, high-level quote from an in-house team. | Detailed repair estimates from multiple vendors, plus an independent, third-party engineering report with root cause analysis. |

| Supporting Docs | Missing policy endorsements or official reports (e.g., Police, DEWA). | Complete insurance policy, official reports, maintenance logs, and a full inventory of damaged items with proof of ownership. |

A strong submission eliminates ambiguity, facilitating the adjuster's role and accelerating the settlement.

Data from Central Bank filings show that well-documented claims with third-party validations achieve an 85% approval rate, compared to just 60% for incomplete submissions. In Dubai, where 59 licensed insurers operate, using specialist support is key. For example, a Grade A office flood claim recovered Dh1.2 million because detailed MEP assessments were provided, cutting downtime by a massive 70% with warranty-backed repairs.

This data underscores a critical point: investing in professional technical documentation delivers a significant return in both claim success rate and recovery speed. Your dossier is not just about showing what was damaged; it is about proving why it failed and how it must be rectified, leaving no room for doubt.

Talking to Your Insurer and Getting to a Fair Settlement

Once the claim dossier is submitted, the process shifts to communication and negotiation. For property management professionals in Dubai, this phase requires a professional, clear, and persistent approach. Engagement with the insurer and their appointed loss adjuster is not merely about answering questions; it is about confidently guiding the conversation toward a fair resolution based on the comprehensive evidence provided.

The primary objective is to maintain a professional, fact-based dialogue. All communications—emails, phone calls, and meetings—should reinforce the strength of your claim. It is crucial to set aside emotion and focus on the policy terms, the evidence, and the technical reports.

Setting the Right Tone From Day One

Your initial interaction establishes the tone for all subsequent engagement. A structured, professional approach prevents miscommunication and creates a clear, auditable trail—a non-negotiable requirement in the UAE's formal business environment.

A simple, effective communication protocol includes:

- Your First Email: Keep it concise and professional. Include the policy number, date and time of the incident, property address, and a brief, one-sentence summary of the damage. State that mitigation measures are underway and a full claim package is being compiled.

- Responding to RFIs: Treat any Request for Information (RFI) from the insurer formally. Respond promptly, reference their specific query, and provide the exact information requested. If a document is unavailable, explain why.

- Proactive Follow-up: If you do not receive an update within a reasonable timeframe, such as 5-7 business days after a major submission, a polite follow-up is appropriate. It demonstrates diligence and ensures the claim remains active.

This organised communication prevents your claim from being deprioritised and ensures all parties are aligned.

Handling the Loss Adjuster's Site Visit

The loss adjuster's site visit is a pivotal moment. Their role is to independently verify the cause and scope of the damage against your claim and policy terms. Your role is to facilitate a smooth, transparent inspection.

Prepare your team for their arrival:

- Designate a Single Point of Contact: Appoint one knowledgeable individual—typically the facility manager or chief engineer—to accompany the adjuster. This ensures informational consistency and prevents conflicting narratives.

- Have All Documentation Ready: Prepare a complete copy of the claim file, available digitally (on a tablet) and in hard copy. This includes maintenance logs, engineering reports, and all photographic evidence.

- Anticipate Key Questions: The adjuster will inquire about the property's maintenance history, the incident timeline, and your immediate response. Your team must provide clear, factual answers supported by your records.

The adjuster is there to answer three questions: "what happened, why did it happen, and how much will it cost?" When you're well-prepared and can walk them through the evidence, showing them maintenance logs before they even ask, the visit feels less like an interrogation and more like a collaborative fact-checking exercise.

Getting Ahead of the Usual Arguments

Disagreements can arise, but many can be preempted with robust documentation. In Dubai, common points of contention relate to causation and valuation.

- "Wear and Tear" vs. Sudden Damage: This is a classic dispute. The insurer may attribute a burst pipe to gradual deterioration (often excluded) rather than a sudden failure. Your strongest defence is a complete set of maintenance logs from your Annual Maintenance Contract (AMC). These records prove diligent upkeep, undermining the "wear and tear" argument.

- Disagreements on Repair Costs: The insurer's initial offer may be lower than your quotations. The solution is to ensure your quotes are highly detailed, itemising all costs: labour, materials, specialist equipment, and overhead. Obtaining two or three comparable quotes from other reputable contractors also strengthens your position by establishing a clear market rate for the required work.

Navigating these discussions is an integral part of the process. For complex claims, engaging professional insurance claim support can be beneficial. By anticipating these friction points and having evidence ready, you transform a subjective argument into a straightforward, fact-based discussion, drastically improving the probability of achieving a fair settlement.

Coordinating Post-Settlement Actions and Repairs

Securing settlement approval is a significant milestone, but it marks the beginning of the recovery phase, not the end. For property and facility managers in Dubai, the focus immediately pivots to executing repairs efficiently, on budget, and to a high standard.

This stage translates the financial settlement into tangible asset restoration and is critically important. Poorly managed repairs can introduce new liabilities, exhaust settlement funds, and diminish the long-term value of the property.

Executing and Documenting the Repair Works

Once you receive authorisation from the insurer, it is time to mobilise contractors. This phase requires the same meticulous attention to detail as the initial claim submission. Active project management is necessary to ensure accountability and prevent scope creep.

The primary objective is to ensure the final repairs align perfectly with the scope of work (SOW) approved by the insurer. Any deviation can lead to budget overruns that will not be covered.

- Vet Your Contractors: Verify that all contractors hold a valid trade licence in Dubai for the specific work being performed and carry adequate public liability insurance. This is non-negotiable.

- Align on the Scope of Work (SOW): Before work commences, conduct a kick-off meeting with the contractor and your FM team. Review the approved repair scope line by line to eliminate any ambiguity about what the settlement covers.

- Continue Documentation: Your evidence-gathering process does not end. Continue to take high-resolution photos and videos before, during, and after the repairs. This creates an undeniable visual record of the restoration, which is invaluable for any future warranty claims.

A common oversight is failing to adequately document the asset's condition after repairs are completed. Final photographs and handover certificates are not mere formalities. They are your proof that the work was completed to the required standard, officially closing the incident file.

Managing Warranties and Finalising the Claim

A frequently overlooked yet critical component is warranty management. Every new piece of equipment—be it a pump, an AC unit, or electrical wiring—should come with a warranty. For example, a new HVAC chiller should have a manufacturer's warranty of 1-2 years, and the contractor should guarantee their installation labour for at least 6-12 months.

Failing to catalogue these warranties is a forfeiture of value. Your facility management team must log all warranty details—start dates, end dates, service contacts—into your asset management system. This simple administrative step protects you from future repair costs if a newly installed component fails prematurely.

Finally, conduct a thorough post-claim review. This is not an exercise in assigning blame but an opportunity to refine internal processes. Convene your team to analyse the entire claim journey, from incident discovery to final handover.

- How quickly did we act to mitigate the initial damage?

- Were there any gaps in our initial documentation?

- How effective was our communication with the loss adjuster?

- Did the settlement fully cover the actual cost of restoration?

Answering these questions will identify weaknesses in your claims protocol. It enables you to update standard operating procedures, enhance staff training, and ensure you are better prepared for future incidents. This transforms a reactive event into a strategic opportunity for operational improvement.

Sidestepping the Common Pitfalls of the Claims Process

Filing a property damage claim in Dubai is not just a procedural task; it is about navigating a process where minor errors can lead to significant delays or rejection. The most common issues that affect asset and facility managers are often not overt blunders but subtle mistakes that compromise a claim's integrity from the start.

The key is to treat the claim as a formal, evidence-based procedure from the moment the damage is discovered. Below are the most common traps and how to avoid them.

The Danger of a Delayed Notification

This is arguably the most critical error: waiting too long to notify the insurer. Most policies in the UAE stipulate a strict window for reporting an incident, typically between 7 and 14 days. The temptation to wait until a full damage assessment is complete is a high-risk strategy.

A delay provides the insurance company with leverage. They can argue that the policyholder failed to act promptly to mitigate further damage or that the scene was compromised over time, making it difficult to assess the original loss.

Consider this scenario: a pipe bursts over a weekend. The incident is not reported for three weeks while quotes are being gathered. The insurer could reasonably argue that the costly mould remediation now required is a consequence of the delay, not the initial leak, and deny that portion of the claim.

Jumping the Gun on Non-Emergency Repairs

There is a fine but critical distinction between prudent mitigation and unauthorised repairs. You have a duty to prevent further loss, which includes stopping a leak, boarding up a broken window, or placing a tarp over a damaged roof. These are immediate, necessary actions.

However, you must not commence full-scale restoration before the loss adjuster has conducted their inspection.

Authorising permanent repairs before the insurer assesses the scene effectively destroys the evidence. For example, if a facility manager disposes of a faulty HVAC unit that caused a major flood before the adjuster's visit, it becomes impossible for the insurer to verify the root cause. This is a direct route to claim denial.

For a deeper analysis, review our guide on why property insurance claims get delayed or rejected in Dubai.

Disorganised and Incomplete Documentation

Submitting a disorganised, incomplete claim file invites delays and intense scrutiny. A random assortment of photos, emails, and unitemised invoices forces the adjuster to act as an investigator, creating friction and raising immediate doubts about the claim's validity.

Every document, from the initial incident report to the final contractor's quotation, must be labelled, dated, and organised chronologically. This presents a clear, compelling narrative that leaves no room for questions.

The quality of your documentation is a direct reflection of your professionalism. A clean, well-structured claim file doesn't just speed things up; it builds credibility. It tells the insurer you're a serious, organised partner in the process.

The stakes are high. Central Bank data reveals that property claims constitute 41% of the Dh11 billion in total insurance payouts. Historically, only 65% of these were settled without litigation. With industry reforms and the adoption of AI to reduce settlement times, collaborating with a technically proficient team that excels in documentation is more critical than ever. It is the most reliable path to a faster, more favourable outcome.

For more on this, you can see the latest UAE insurance industry performance analysis.

Got Questions? Here Are Some Straight Answers

When managing property damage, numerous questions arise. During a stressful period, clear, practical answers are essential. Here are some of the most common queries from facility and asset managers across Dubai, along with our professional guidance.

"How Long Do I Have to Tell My Insurer?"

This is a critical deadline that cannot be missed. Most insurance policies in the UAE specify a narrow window for reporting an incident—typically between 7 and 14 days.

Failure to meet this deadline can result in the rejection of your entire claim. The best practice is to notify your insurer or broker in writing as soon as it is safe to do so. Do not wait until you have a complete damage report; submit the initial notification immediately.

"Can I Start Fixing Things Before the Insurance Adjuster Arrives?"

Yes, you can—and you must. You have a legal duty to mitigate the damage, which means taking reasonable steps to prevent the situation from worsening. You should authorise temporary, urgent fixes, such as engaging a plumber to stop a major leak or boarding up a shattered window to secure the property.

However, do not begin any permanent repairs or dispose of any damaged items. The loss adjuster must be able to inspect the full extent of the damage to validate your claim. Replacing a ruined carpet before their visit is tantamount to destroying evidence. Document every mitigation step with photographs and retain all related invoices.

The biggest mistake we see is people confusing mitigation with restoration. Mitigation is the emergency stop-gap—it’s about stopping the bleeding. Restoration is the full repair job. You only move ahead with mitigation before the insurer gives the green light. Doing so shows you're a responsible manager, but it doesn't mess up the claims process.

"How Does My AMC Help with an Insurance Claim?"

Your Annual Maintenance Contract (AMC) is one of your most valuable documents when filing a claim. It serves as proof that the property has been professionally maintained.

From an insurer's perspective, a common basis for denying a claim is attributing the damage to neglect or pre-existing wear and tear. Your AMC records—including maintenance logs, service reports, and condition assessments—provide a robust defence against this argument. They offer clear, irrefutable evidence of due diligence, which almost always leads to a smoother, faster, and more successful claim outcome.

At SnapFixNow, we specialise in providing the technical support required for insurance claims. We deliver the detailed engineering reports and robust documentation that strengthen your submission and help accelerate your settlement. Find out more at https://www.SnapFixNow.com.