For facility and property managers in Dubai, indisputable technical proof is the new language of insurance. The days of filling out a simple form are long gone. Insurers now expect a full dossier of verifiable evidence—from timestamped photos to detailed engineering reports—before they’ll even consider a property damage claim.

Getting this documentation right isn't just a box-ticking exercise anymore. It’s absolutely critical to protecting your assets.

Why Insurers in Dubai Demand Hard Technical Proof

The ground has completely shifted under the insurance claims process here in Dubai. Not long ago, a straightforward claim form with a few basic photos might have been enough to get the ball rolling. Today, insurers are scrutinising every detail, demanding solid, technical evidence to back up every part of a property damage claim.

This isn't a random change. It's a direct, calculated response to the massive financial hit the industry took after catastrophic weather events rewrote the region's risk profile. For you, this new reality means the burden of proof has grown immensely. Your insurer is looking for a professional, data-driven case file, not just a simple request for money.

The Financial Fallout from Record-Breaking Storms

The real turning point was the series of severe storms that battered the UAE. In the aftermath of the unprecedented heavy rains, UAE insurers were left reeling from staggering losses—estimated at up to $2.5 billion (Dh9.175 billion). The bulk of this came from damage to roughly 100,000 vehicles and thousands upon thousands of properties.

This was a cataclysmic event that forced a total rethink of risk and exposure. In the first quarter of the following year, the numbers told the story: gross paid insurance claims shot up by 18.3% year-on-year to Dh11 billion. Property and liability claims alone accounted for Dh4.5 billion, or over 40% of the total payout, a direct consequence of the storm's lingering impact. You can dig deeper into the data with this Khaleej Times analysis.

When you're facing multi-billion dirham losses, you have no choice but to tighten the ship. Insurers moved from a model of trust-based assessments to one that demands verifiable, technical proof to control future payouts and weed out illegitimate claims.

What This New Standard Means for You

This industry-wide pivot has a direct impact on how you need to manage and document every single property incident. Insurers aren't just asking "what happened?" anymore. Now, the question is "can you prove it?"

Your ability to present clear, organised, and technically sound evidence has become the single most important factor determining whether your claim gets paid.

This guide is built to give you the practical, on-the-ground knowledge to meet these new, tougher expectations. We’ll walk through:

- The specific kinds of technical proof insurers in Dubai are now demanding.

- How to capture photo and video evidence that will stand up to intense scrutiny.

- The right way to compile technical reports, test data, and credible repair estimates.

- The common pitfalls that get claims rejected and, more importantly, how to avoid them.

In Dubai's new risk environment, mastering the art of documentation isn't just good practice—it's essential for keeping your business running and protecting your bottom line.

Building Your Irrefutable Evidence Portfolio

A successful insurance claim is won or lost long before you submit the paperwork. It’s built on the strength of the evidence you gather, starting from the very moment an incident occurs. For property and facility managers in Dubai, assembling this portfolio isn't just an administrative task—it's a critical part of protecting your asset. The goal is to create a clear, chronological story of the damage that leaves no room for doubt.

Think of the first few hours after damage is discovered as the "golden hour" for documentation. What you capture during this period often becomes the most compelling technical proof your insurer needs to see. Swift, methodical action here can be the difference between a quick approval and a lengthy, frustrating rejection.

Mastering Immediate Documentation Protocols

The moment you're alerted to an issue—whether it's a burst pipe, a storm-damaged roof, or a malfunctioning HVAC unit causing water ingress—your first priority is safety. Immediately after that comes documentation. Your team needs a clear, rehearsed protocol for capturing evidence before anything is moved, repaired, or cleaned up.

This initial evidence serves as your baseline, proving the immediate aftermath of the event. Insurers are particularly interested in seeing the damage in its raw, unaltered state.

To meet this standard, your documentation should always include:

- High-Resolution Photographs: Get wide shots of the affected area to establish context, then move in for detailed close-ups of the damage itself. Don't forget to photograph serial numbers on damaged equipment, water level marks on walls, and any specific points of failure.

- Timestamped and Geotagged Video: A continuous video walkthrough is incredibly powerful. As you film, narrate what you're seeing, showing the extent of the damage from multiple angles. Modern smartphones automatically embed date, time, and location data, which adds a layer of authenticity that insurers really value.

- Detailed Notes: Photos are vital, but written notes fill in the gaps. Document smells (like smoke or mould), sounds (like dripping water), and any initial observations from your team. A simple log of who discovered the issue and when can be invaluable down the line.

This structured approach makes collecting proof much simpler, which is a key part of providing the insurance claim support insurers in Dubai expect.

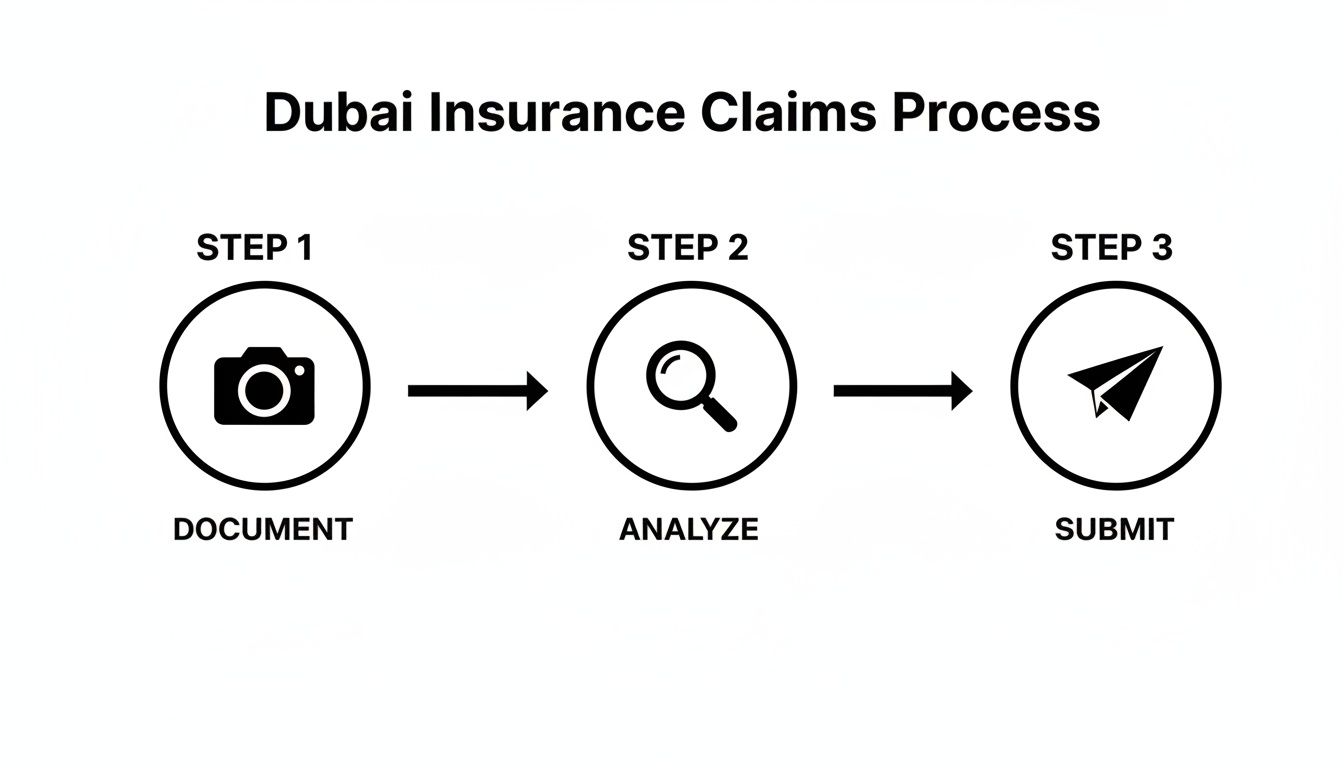

This workflow shows the essential steps for a successful claim: documenting the incident, analysing the evidence, and then submitting a complete package. An organised approach like this ensures you don't miss a critical step, strengthening your position with the insurer right from the start.

The Power of Pre-Incident Records

While immediate documentation shows the after, pre-incident records establish the before. An insurer’s first question is often about the condition of the property prior to the loss. Without solid proof of its previous state, they might argue that the damage was pre-existing or resulted from poor maintenance.

Your best defence against this is a well-organised library of historical data. This is where diligent facility management truly pays off.

An adjuster's job is to verify the loss. If you provide them with clear maintenance logs, recent inspection reports, and pre-incident photos, you're not just making a claim; you're confirming a fact. This shifts the conversation from one of doubt to one of validation.

Key pre-incident documents include:

- Routine Maintenance Logs: Records of HVAC servicing, plumbing inspections, and electrical system checks demonstrate due diligence.

- Previous Inspection Reports: Regular property checks, like those detailed in guides for commercial building assessments, establish a documented history of the asset's condition.

- Capital Improvement Records: Invoices and plans for recent upgrades or renovations prove that systems were modern and well-maintained.

- Archival Photos and Videos: Annual or quarterly photographic records of key areas (roofs, plant rooms, facades) provide an undeniable visual baseline.

Organising Your Evidence into a Compelling Narrative

Once you've gathered both immediate and historical evidence, the final step is to assemble it into a logical, easy-to-follow story for the loss adjuster. A disorganised folder of random files will only create confusion and delays. Your submission should be structured like a professional report.

Create a master digital file for the claim, organised into clear subfolders:

- Incident Report: A summary document outlining the date, time, location, and nature of the incident.

- Immediate Evidence (Dated): All photos and videos from the "golden hour," organised chronologically.

- Pre-Incident Condition: Maintenance logs, inspection reports, and archival photos.

- Communications Log: A running record of every conversation with the insurer, broker, and any contractors.

- Technical Reports & Quotes: This folder is where you'll keep the expert analyses and repair estimates you gather next.

By building this comprehensive portfolio, you provide the clear, verifiable, and technical proof your insurer is looking for. You go from being a claimant asking for funds to a professional partner presenting a documented case for restoration. This makes a swift and fair settlement far more likely.

Crafting a Compelling Technical Report

Think of your photos and videos as the opening scene of a movie—they grab attention and show what happened. But the technical report? That’s the script. It’s where you build your case, and for insurers in Dubai, this document is the absolute centrepiece of your claim.

It needs to be more than just a laundry list of broken items. Your report has to be a precise, diagnostic tool that gives the loss adjuster a crystal-clear and logical path from cause to cost. A weak or vague report is an open invitation for scrutiny, endless questions, and delays. A strong one, however, gives the insurer the confidence to sign off on the claim. Quickly.

This isn't just about describing damage. It's about building an airtight argument, backed by solid evidence, that justifies every single dirham you’re claiming.

Moving Beyond Simple Descriptions

An insurer’s desk is piled high with reports. A generic line like "water damage in the basement" is completely unhelpful and immediately raises red flags. It tells them nothing. Your report has to dig deeper, answering not just what was damaged, but how and, most importantly, why.

You have to deconstruct the incident. This means a proper root cause analysis, a precise scope of the damage, and metrics that an adjuster can actually understand and verify.

Put on your engineer's hat. The goal is to create a document so clear and well-supported that it answers the adjuster's questions before they even have a chance to ask them.

The Anatomy of an Approved Report

From my experience, technical reports that get the green light in Dubai almost always follow a specific structure. Each section logically builds on the last, creating a story that’s easy to follow and hard to dispute.

Make sure your report includes these core elements:

- Executive Summary: A punchy, one-page overview. What happened, what caused it, how bad is the damage, and what’s the estimated repair cost? This is for the busy decision-maker who just needs the highlights.

- Incident Timeline: A step-by-step, chronological account. From the moment the problem was found to when the site was made safe, include dates and times for every key action.

- Root Cause Analysis: This is where you get forensic. A detailed investigation into the specific point of failure. Honestly, this is probably the most critical part of the entire report.

- Scope of Damage Assessment: An itemised list of every single affected asset, system, or structure. Be descriptive and include supporting photos for each item.

- Quantifiable Impact Data: Hard numbers. You need to translate the damage into metrics the insurer can process.

This structure is the foundation of effective insurance claim support in Dubai. It aligns perfectly with how adjusters are trained to evaluate a loss, making their job easier—which is always a good thing.

Conducting a Thorough Root Cause Analysis

Your insurer needs to be 100% certain that the cause of the loss is actually covered by your policy. A shallow analysis just creates more work for them, which means delays for you. You have to nail down the exact source of the problem.

For instance, don't just say "a pipe burst." A proper root cause analysis would state: "A 2-inch copper supply line for the chilled water system failed at a soldered elbow joint in the ceiling void of Unit 702, likely due to long-term corrosion." See the difference? That level of detail, especially when backed by a photo of the failed joint, is almost impossible to argue with.

An insurer's main job is to validate the 'proximate cause' of the loss. When you provide a clear, evidence-backed root cause analysis, you're essentially doing their homework for them. This builds trust and speeds up the approval process like nothing else.

This section needs to connect the dots for the insurer, proving that the failure was sudden and accidental, not the result of negligence or old wear and tear that should have been addressed earlier.

Quantifying Damage in an Insurer's Language

Vague descriptions of damage are a nightmare for an insurer to put a price on. To provide the technical proof your insurer expects, you must translate the damage into concrete, measurable units. This removes all the guesswork and gives them a solid basis for the repair quotes you’ll be submitting.

Here are a few real-world examples of what I mean:

- Instead of: "The roof leaked badly during the storm."

Use: "Water ingress was measured at an estimated 150 litres per hour at the peak of the storm, affecting 75 square metres of the top-floor office space." - Instead of: "The main AC unit is broken."

Use: "The primary chiller (Model XYZ-123) experienced a catastrophic compressor failure, resulting in a total loss of 250 tonnes of cooling capacity." - Instead of: "The fire damaged the electrical room."

Use: "The fire caused thermal damage to 12 circuit breakers and melted the insulation on 40 linear metres of feeder cables, rendering the main distribution board inoperable."

This is so important. Quantifying the damage allows the adjuster to apply standard industry costing models to your claim, making the whole valuation process transparent and much faster. When you use specific technical language and data, you show that you're a professional who understands your assets. That alone adds a huge amount of credibility to your report and your entire claim.

Getting Your Repair Quotes Right

Once your technical report is in, the next hurdle is money. Insurers in Dubai are pros at sniffing out padded or vague repair estimates. If your quote looks like it was pulled out of thin air or is just one big number, you're practically inviting the insurer to hit the brakes on your claim.

Your job here is to hand them a set of quotes that are crystal clear, broken down to the last fil, and perfectly matched to the damage you've already proven. This isn't just about getting a price; it's about building a rock-solid financial case that’s easy to say "yes" to.

Sourcing Quotes from Contractors Insurers Trust

First things first, you need quotes from reputable, licensed contractors. An insurer gives a lot more weight to an estimate from a well-known, certified company than one from a random handyman found online.

Always get at least two or three quotes from different companies. It shows you’ve done your homework and are looking for fair market pricing, not just taking the first number thrown at you.

When picking contractors, make sure they tick these boxes:

- Properly Licensed and Certified: They absolutely must have the right trade licenses from the Dubai Department of Economy and Tourism (DET) and any other necessary technical certifications.

- The Right Experience: If you have a complex HVAC issue, you need an HVAC specialist, not a general maintenance company. Their track record should match the job.

- Insured and Compliant: Check that they have their own liability insurance and follow local building codes. It’s a must.

An insurer sees your choice of contractor as a reflection of your own diligence. Handing them quotes from properly vetted specialists tells them you're managing the situation responsibly. That builds trust and can seriously speed things up.

The Anatomy of a Quote That Won't Get Questioned

A winning quote is all about the details. A single lump-sum figure is a red flag and will get bounced back almost every time. Each quote needs a meticulous, itemised breakdown so the loss adjuster knows exactly what every dirham is for.

A credible quote must break down these three key areas:

- Labour Costs: This needs to be detailed. Think: senior electrician, 20 hours at AED X per hour; plumber, 15 hours at AED Y per hour.

- Material Costs: List every single thing. From big-ticket items like pumps and chillers down to the specific type of cable, pipes, and paint. Include quantities, unit costs, and specs.

- Equipment Costs: If the job needs special gear like a crane, scaffolding, or specific diagnostic tools, list these as separate line items with their rental or usage fees.

When you provide this level of detail, the quote stops being a simple price and becomes a transparent financial document that can be checked against industry standards.

Tying the Quote Directly to Your Technical Report

This is where so many claims stumble. Your repair quotes must be a perfect mirror of what’s in your technical report. Any mismatch creates confusion and gives the insurer a reason to push back.

If your report documents damage to 40 linear metres of a specific cable, the quote must show the cost for exactly 40 metres of that same cable. It’s that simple.

This direct link proves the money you’re asking for is tied directly to the damage you’ve documented. It shuts down any arguments that you're trying to fix pre-existing issues on their dime. For big jobs with multiple contractors, using a service that streamlines third-party contractor management can be a lifesaver, ensuring all your quotes tell the same consistent story.

One last tip: a smart quote anticipates the unknown. You can include a "provisional sum" for things you can't see yet. For example, if you're fixing water damage, you might add a provisional sum for replacing structural supports that can only be assessed after the walls are opened up. Justifying this upfront shows the insurer you’ve thought ahead, which only strengthens your case for a fair settlement.

Of course. Here is the rewritten section, crafted to sound completely human-written and natural, following all the specified requirements.

Navigating Timelines and Regulatory Hurdles

Even if your technical evidence is perfect, an insurance claim in Dubai can still get stuck. It’s a common frustration. You’ve got all the proof, but procedural missteps—either with municipal regulations or the insurer's own internal rules—can derail everything. Think of it as a dual-track system; a delay on one track almost always creates a bottleneck on the other, putting your entire settlement at risk.

The trick is to stop thinking of compliance as a separate chore. Instead, treat it as a critical part of your evidence portfolio. From getting the right permits before a hammer swings to keeping a clear line of communication open, every procedural step you take needs to be documented and shared with your insurer. This proactive approach is what stops a claim from being rejected on a frustrating, and entirely avoidable, technicality.

Securing Essential Permits and Approvals

Before any major repair work kicks off, you almost always need a green light from local authorities. For most property repairs here in Dubai, that means getting a No Objection Certificate (NOC) or a specific permit from bodies like Dubai Municipality or the relevant free zone authority.

Trying to jump the gun and start repairs without these approvals is a recipe for disaster. The consequences can be severe:

- Work Stoppage Orders: Authorities can bring your project to a dead halt, causing massive delays.

- Fines and Penalties: Skipping the proper channels can lead to some hefty financial penalties.

- Claim Invalidation: This is the big one. Many insurance policies have clauses that flat-out void your coverage if repairs are done in violation of local laws.

Your insurer is going to ask for copies of these permits. It’s a standard part of their due diligence. By getting them sorted and documented from the very beginning, you’re providing the technical proof your insurer expects to see—proof that the entire repair process is legitimate, compliant, and being handled professionally.

A mistake I see all the time is assuming emergency repairs are exempt from all the rules. While you might be allowed to do some initial stabilisation work, always double-check the requirements with the relevant authority. And critically, keep your loss adjuster in the loop on every single action you take.

Mastering the Claims Timeline and Communication

The insurance market here is growing incredibly fast. Dubai International Financial Centre (DIFC) just announced a massive 35% jump in gross written premiums for insurance and reinsurance, hitting USD 3.5 billion in a single year. This isn't just a number; it shows how much of a major insurance hub Dubai has become. For you, it means insurers are under more pressure than ever to process claims efficiently, often leaning heavily on digital tools and crystal-clear evidence. Proactive communication has gone from being a nice-to-have to an absolute necessity. You can read more about Dubai's evolving insurance landscape.

A typical claim moves through several key stages, and honestly, any one of them can become a sticking point:

- First Notice of Loss (FNOL): This is your initial report of what happened.

- Adjuster Assignment and Site Visit: An independent loss adjuster is brought in to assess the damage firsthand.

- Submission of Technical Proof: You hand over your full evidence package—reports, photos, videos, quotes, the works.

- Review and Negotiation: The adjuster goes through your submission and will likely come back with questions or requests for clarification.

- Settlement and Payment: Your claim gets the final approval, and the funds are released.

To keep things moving and avoid getting stuck in a bottleneck, get into a regular communication rhythm with your broker and the loss adjuster. A simple weekly check-in email that summarises progress, highlights any outstanding actions, and confirms the next steps creates a documented timeline. This kind of proactive engagement in providing insurance claim support in Dubai does more than just show you're diligent; it ensures your claim doesn’t get buried on a busy adjuster’s desk, keeping it on track for a much faster resolution.

Using Technology for a Streamlined Claim Process

Relying on old-school, manual processes for insurance claims is a recipe for errors, delays, and a whole lot of frustration. To provide the clear, technical proof that insurers in Dubai demand, a modern workflow isn't just nice to have—it's essential. The right technology and professional support can completely change your approach, turning a chaotic process into a predictable one.

Take photo-based work order platforms, for example. They create an automatic, unalterable evidence locker that insurers love. Every single photo and video is timestamped and geotagged, building an irrefutable chain of custody from the moment a problem is reported to the final sign-off. This digital trail eliminates any arguments over when the damage happened or the asset's condition beforehand.

This shift towards digital proof is happening for a reason. The UAE's insurance market is expanding fast. With gross written premiums projected to hit US$10.04 billion and claims payouts climbing a staggering 18.3% year-over-year in a single quarter, insurers are tightening their requirements to manage risk. Providing clear, tech-enabled evidence is now central to navigating this stricter environment. You can explore more about the UAE's insurance market trends to see the bigger picture.

The Credibility of Certified Technicians

Of course, technology is only one part of the equation. The credibility of the person assessing the damage is just as important, if not more so. A DIY assessment from your in-house team, however skilled they may be, simply doesn't carry the same weight as a report from an independent, ISO-certified technician.

An insurer's goal is to validate the claim with objective, third-party evidence. When a certified technician signs off on a root cause analysis, it removes doubt and answers the insurer’s key questions before they even have to ask.

This combination of people, process, and technology creates a powerful workflow for insurance claim support in Dubai. It not only meets the insurer's demands for verifiable proof but also saves your team a massive amount of time. You can learn more about how technology-enabled maintenance fundamentally improves operational efficiency and documentation across the board.

By adopting a modern approach, you move from simply filing a claim to presenting a professional, data-driven case. This proactive stance reduces the stress, minimises the back-and-forth, and ultimately leads to faster, more successful settlements. That means getting your property back to full operation without unnecessary delay.

Frequently Asked Questions

What's the Single Biggest Mistake to Avoid in a Dubai Insurance Claim?

Hands down, it's submitting incomplete or poorly organised evidence. You have to remember, insurers in Dubai operate on a "prove it" basis. A messy file with missing photos, reports that don't add up, or mismatched quotes immediately raises red flags and brings everything to a halt.

Make sure every single piece of technical proof is crystal clear, laid out chronologically, and directly supports your claim right from the start.

How Long Does a Typical Property Damage Claim Take to Settle?

It really varies, but a well-documented claim can often be settled in just a few weeks. The ones that drag on for months are almost always bogged down by insufficient technical proof or problems with regulatory compliance.

Being proactive and giving the insurer the exact technical proof they expect is the fastest way to get things moving.

Can I Start Emergency Repairs Before the Insurer Approves?

Yes, and you absolutely should. If you have a leak or a damaged roof, your priority is to prevent further damage. Take immediate steps to stop the problem.

The key is to document everything with photos before and after you take those emergency actions. However, don't even think about starting the full-scale, permanent repairs until you have the green light from your loss adjuster. Doing so could put your entire claim at risk.

Providing robust insurance claim support in Dubai means documenting every single step, especially the urgent ones.

Ready to build an airtight case for your next insurance claim? SnapFixNow provides certified technicians and a photo-based platform to capture the indisputable technical proof your insurer demands, ensuring a faster, smoother settlement. Learn more about our services.