When property damage disrupts operations, the initial decisions made by facility managers, asset owners, or procurement teams can significantly impact financial recovery. Two critical but often confused concepts are "insurance claim support" and a "contractor quote." While both relate to asset restoration, they serve fundamentally different objectives within a UAE commercial context.

Insurance claim support is a strategic financial recovery service. Its primary function is to compile a comprehensive, evidence-based dossier to substantiate a claim and maximize the financial settlement from an insurer. This involves root cause analysis, technical reporting, and adherence to policy requirements.

A contractor quote is a tactical operational document. Its scope is limited to the direct costs of labour and materials required to execute a specific repair. The goal is to restore asset functionality as quickly and efficiently as possible.

Defining The Core Difference For UAE Property Managers

For decision-makers managing commercial, hospitality, retail, or industrial assets across the UAE, distinguishing between these two functions is crucial for mitigating financial risk and ensuring operational continuity. A contractor's quote facilitates the physical repair, but robust insurance claim support ensures the full financial burden of the incident—including consequential losses—is recovered under the terms of the insurance policy.

Understanding the formal, evidence-based nature of navigating the property insurance claims process is the first step. It is not merely a request for funds but a structured procedure demanding rigorous proof.

This distinction has gained prominence following major weather events, such as the April 2024 storm, which caused an estimated USD 8 billion in economic losses. With projections from firms like Swiss Re indicating a 6% rise in Middle East non-life premiums for 2025, insurers' scrutiny of claims is intensifying. For asset managers, a disciplined approach to claims is now a financial imperative.

At-a-Glance Comparison: Financial Recovery vs. Operational Repair

This framework outlines the fundamental differences for UAE asset and facility managers who must make informed, timely decisions. One function is designed for financial recovery, the other for operational restoration. Effective financial recovery begins with understanding the technical proof your insurer expects.

| Attribute | Insurance Claim Support | Direct Contractor Quote |

|---|---|---|

| Primary Goal | Maximise financial settlement from the insurer in line with policy terms. | Restore asset functionality through defined repair work. |

| Provider Type | Specialised technical consultants or certified FM companies with claim expertise. | MEP, civil, or specialised repair contractors. |

| Focus Area | Financial recovery, risk mitigation, and compliance with insurance policy conditions. | Operational continuity, problem resolution, and asset uptime. |

| Key Deliverable | Insurer-grade technical report, root cause analysis, and evidence dossier. | Detailed scope of work (SOW) and cost proposal for a specific task. |

| Cost Structure | Typically a percentage of the approved claim value (e.g., 5-10%) or a fixed fee. | Fixed price or time-and-materials basis for labour and parts. |

| Success Metric | Value of approved claim vs. total documented financial loss incurred. | Speed, quality, and cost-effectiveness of repair execution. |

Ultimately, a contractor quote quantifies the cost to fix the immediate, visible problem. Insurance claim support builds the comprehensive, evidence-backed case required to prove the full financial scope of the loss to an insurer, preventing uncovered expenditures.

Comparing Strategic Goals and Operational Scope

While both an insurance claim and a contractor quote address asset damage, their strategic objectives and operational scopes are distinct. One is a financial instrument for loss recovery; the other is a tactical tool for operational remediation.

Insurance claim support focuses on constructing a robust case for a comprehensive financial settlement. Its scope is intentionally broad, encompassing not only the visible damage but also a detailed root cause analysis. The deliverable is a set of meticulous, insurer-ready reports that justify the full financial extent of the loss, thereby protecting the asset owner's balance sheet.

Conversely, a contractor quote is designed for execution speed. Its scope is narrow and precise, focused exclusively on the labour, materials, and timeline required for a specific repair. Whether for a plumbing, electrical, or HVAC failure, the objective is purely operational: restore function and minimise downtime.

The Financial Recovery vs. Operational Continuity Balance

For property managers in the UAE, this creates a critical decision point between long-term financial recovery and immediate operational stability. In a high-stakes commercial environment where downtime directly translates to revenue loss and tenant dissatisfaction, this balance is key. Prioritising only the quick fix restores operations but may leave the asset owner liable for the full financial consequences.

The tension between these priorities was highlighted by the April 2024 floods. The event triggered an estimated USD 8 billion in economic losses, with an insurance coverage gap of approximately USD 5 billion. This demonstrates the significant financial exposure for asset owners who lack the structured claim support needed to secure recovery. You can learn more about how these events impact the market in the full customer claims report.

For procurement teams and facility managers, the key distinction is this: a contractor's quote answers, "What is the cost to repair?" while insurance claim support answers, "What is the total quantifiable financial impact, and how do we prove it to our insurer?"

Scope Comparison Across Property Types

The practical application of these approaches varies significantly by asset type, particularly when engaging specialist providers like MEP contractors in Dubai.

- Commercial & Retail: In a mall or office tower, business interruption is a primary driver of financial loss. A contractor's quote will focus on restoring MEP systems to resume operations. A comprehensive insurance claim scope extends further, documenting lost revenue, tenant compensation costs, and damage to inventory to build a complete financial case.

- Hospitality: In a hotel, guest experience is paramount. A contractor quote will prioritise discreet, minimal-disruption repairs, often scheduled during off-peak hours. The insurance claim scope, however, expands to quantify the costs of relocating guests, potential brand reputation damage, and the replacement value of specialised, high-end fixtures and equipment.

- Industrial: In a factory or logistics centre, a contractor quote may address a single equipment failure, like a faulty pump or electrical panel. The insurance claim support, however, adopts a wider perspective, analysing production downtime, spoilage of raw materials, and potential contractual penalties for supply chain disruptions.

Evaluating Documentation and Evidence Standards

The most significant divergence between insurance claim support and a contractor quote lies in the documentation and evidence standards. One is a transactional proposal; the other is a forensic evidence package designed to withstand scrutiny from loss adjusters and legal counsel.

For procurement and property managers, understanding this distinction is fundamental to managing administrative overhead and mitigating compliance risk.

A standard contractor quote is direct and functional. The documentation is minimal, focusing on a clear scope of work, a bill of materials, labour costs, and payment terms. Its purpose is to secure approval for work to commence. It does not need to justify the root cause of the damage.

In contrast, documentation for insurance claim support is designed to build an irrefutable case for financial recovery. The process is meticulous, often adhering to quality management systems like ISO 9001:2015 to ensure credibility, which is particularly vital for complex Mechanical, Electrical, and Plumbing (MEP) damage claims.

Insurer-Grade Evidence Requirements

The objective of claim support is to anticipate and proactively answer every potential question from an insurer. This requires a comprehensive evidence package that eliminates ambiguity.

A typical dossier includes:

- Detailed Technical Reports: These go beyond a simple damage description to provide a root cause analysis, supported by a time-stamped photographic log and a clear, chronological narrative of the incident.

- Asset Condition Assessments: Maintenance logs, service histories, and pre-incident inspection reports are used to prove the asset was in good working order prior to the loss event, countering potential arguments of negligence or pre-existing wear and tear.

- Third-Party Verifications: To strengthen a claim, specialist reports, material lab testing results, or sworn statements may be included. Legal instruments like affidavits are critical for substantiating facts. You can learn more by understanding affidavits as evidence.

The core principle is simple: a contractor quote documents the solution, whereas an insurance claim support package documents the problem in exhaustive, legally defensible detail.

This level of rigor is not optional; it is essential for claim validation. For further insights, decision-makers can review what evidence do insurance loss adjusters look for during site inspections to align internal processes with industry expectations. The difference is not the quantity of documents, but the strategic purpose and forensic quality of the evidence produced.

Breaking Down Timelines and Costs in the UAE

In Dubai's fast-paced commercial environment, downtime directly impacts revenue. The timelines and cost structures for an insurance claim versus a direct contractor quote are fundamentally different, reflecting their distinct objectives of financial precision versus operational speed.

An insurance claim is a structured, multi-stage process governed by procedural requirements. It is a marathon, not a sprint. Work cannot commence until a loss adjuster has conducted a site inspection, the insurer has formally accepted liability, and a settlement has been approved. This deliberate process can result in an asset remaining non-operational for an extended period.

A contractor quote, by contrast, is designed for immediate action. Upon approval, technicians can often be mobilised within hours. It is the appropriate solution for urgent repairs where restoring business operations is the overriding priority.

Comparative Timeline Benchmarks

Understanding expected timelines is crucial for managing stakeholder and tenant expectations. While incident-specific variables exist, the following benchmarks are typical for the UAE market.

The Insurance Claim Process:

- Incident Reporting & Initial Documentation: Must be completed within 24-48 hours of discovery.

- Loss Adjuster Site Inspection: Typically scheduled within 5-10 business days.

- Claim Review & Approval: This stage is the most variable, often taking 3-6 weeks but can extend significantly for complex claims exceeding AED 250,000.

The Direct Contractor Route:

- Quote Submission: For standard MEP issues, a quote can usually be provided within 24 hours.

- Work Commencement: For emergency repairs, mobilisation often occurs within 24-72 hours of quote approval.

The trade-off is clear: a contractor offers rapid operational recovery, while an insurance claim facilitates financial recovery over a longer timeframe. The choice depends on whether the primary need is to resolve an immediate operational issue or to manage a long-term financial liability.

Differentiated Cost Models and Financial Impact

The financial implications of each path are equally distinct. Claim support is a mechanism for recovering incurred losses, whereas a contractor quote represents a direct operational expenditure (OPEX).

Insurance claim support is typically structured in one of two ways: a fixed fee for report generation and case management, or more commonly, a success fee based on a percentage (e.g., 5-10%) of the final claim settlement. This aligns the provider's incentive with the asset owner's goal of maximising recovery.

A contractor quote is a direct cost for labour and materials. In this context, an Annual Maintenance Contract (AMC) provides a significant financial advantage. AMCs usually secure preferential labour rates that are 15-25% lower than ad-hoc call-out charges, enabling better OPEX control and ensuring a rapid response from a vetted service provider.

These financial decisions are being made within a growing UAE insurance market. According to BADRI Consultancy's Q1 2025 analysis, gross written premiums increased by 21% year-over-year, with leading listed insurers reporting a 54% surge in net service results. These figures are available in the full Q1 2025 performance analysis.

A Decision Framework for Choosing the Right Approach

Selecting the optimal path between insurance claim support and a direct contractor quote requires a structured assessment of the incident. For property managers, asset owners, and procurement teams in Dubai, this decision must align with operational priorities, financial thresholds, and insurance policy terms. The correct approach is dictated by the specific variables of the loss event.

This framework is designed to transition decision-making from reactive crisis response to a calculated, defensible strategy. By evaluating key factors, managers can determine whether the priority is immediate operational restoration or comprehensive financial recovery.

Scenario-Based Decision Making

Consider two common scenarios in the UAE's commercial property landscape. These examples illustrate how the scale and complexity of damage should inform the response strategy.

Scenario 1: Minor, Localised Damage (Below Policy Excess)

An isolated HVAC unit in a commercial building fails due to component wear. Business continuity is not affected, and the estimated repair cost is below the typical policy excess of AED 10,000.

Optimal Approach: A direct contractor quote. This path offers speed and cost-efficiency, resolving the issue within hours and treating it as a standard operational expense, thereby avoiding the administrative burden of the insurance process.Scenario 2: Widespread, Complex Damage (Above Policy Excess)

Following a major storm, a hotel's basement-level MEP plant room experiences significant water ingress. The damage affects chillers, pumps, and main electrical panels, causing a major business interruption. The estimated loss significantly exceeds AED 150,000, and the root cause requires technical investigation.

Optimal Approach: Comprehensive insurance claim support. This is non-negotiable to ensure meticulous documentation is prepared for a full financial recovery covering direct repairs, business interruption losses, and potential long-term asset degradation.

A Matrix for Evaluating Your Options

To formalise this process, use this decision matrix to evaluate the incident against four critical pillars. This scoring will clarify whether the primary need is a tactical repair or a strategic financial recovery.

| Decision Factor | Low Score (Favors Contractor Quote) | High Score (Favors Claim Support) |

|---|---|---|

| Damage Scale & Complexity | Isolated, single-asset failure (e.g., one leaking pipe). | Widespread, multi-system damage (e.g., post-flood electrical system failure). |

| Estimated Repair Cost | Below the insurance policy's excess (deductible), typically under AED 15,000. | Significantly exceeds the excess, often above AED 50,000. |

| Business Continuity Impact | Minimal disruption; operations can continue with minor workarounds. | High impact; significant downtime, revenue loss, or tenant displacement is likely. |

| Documentation Requirements | A simple scope of work and invoice are sufficient for internal approval. | Insurer-grade technical reports, root cause analysis, and photographic evidence are mandatory. |

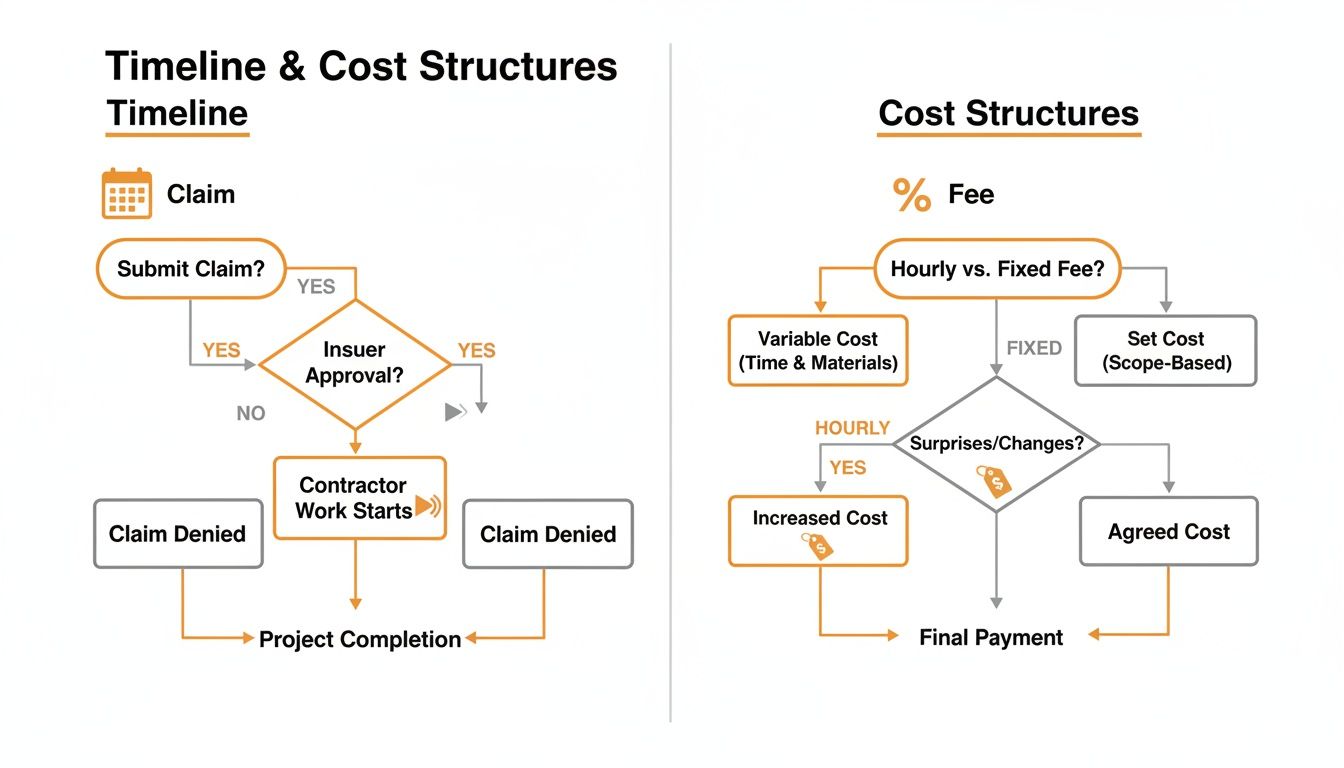

The infographic below illustrates the distinct pathways for timelines and cost structures, highlighting the direct, fast-track nature of a contractor versus the methodical, fee-based approach of a claim.

This visual contrast reinforces the core trade-off: a contractor quote prioritises operational speed, whereas claim support prioritises financial diligence over a longer timeframe. By applying this structured framework, managers can make logical, defensible decisions that protect both asset functionality and financial interests.

Got Questions? We’ve Got Answers for UAE Facility Managers

Even with a clear framework, specific situations can create ambiguity. Here are common questions from facility and property managers across the UAE, with practical answers to help navigate the boundary between a contractor quote and a formal insurance claim.

Can I Just Use My Go-To Maintenance Company’s Quote for My Insurance Claim?

Yes, obtaining a detailed quote from a trusted, certified facility management company is a prudent first step. It provides a credible, third-party benchmark for the anticipated cost of repairs.

However, a standard one-page quote is insufficient for an insurance claim. The insurer's loss adjuster will conduct an independent assessment. To be effective, your contractor's quote must be comprehensive, supported by photographic evidence, technical specifications, and a detailed scope of work. It serves as your initial evidence in the negotiation; a well-documented quote from a reputable firm gives the adjuster a credible basis for their evaluation.

When Does It Make Sense to Pay for Professional Insurance Claim Support?

Professional claim support is a strategic investment for complex, high-value claims where the risk of underpayment is significant.

In the UAE market, a general threshold for engaging professional support is for damages exceeding AED 50,000. This is particularly relevant for incidents involving critical MEP systems, structural issues, or specialised equipment where root cause analysis is complex. While a fee is associated with this service, it is often offset by achieving a higher and more expedient settlement, while also relieving the in-house team of a substantial administrative burden.

Is This Kind of Damage Covered by My Annual Maintenance Contract (AMC)?

This depends entirely on the specific terms and exclusions within your Annual Maintenance Contract (AMC). The majority of standard AMCs are designed for preventive maintenance and addressing routine operational failures. They almost universally contain clauses that exclude damage from external events such as floods, fires, or major accidents, often categorised under force majeure or acts of God.

Nevertheless, your AMC provider remains a critical partner. Even if the repair is not covered under the contract, they are best positioned to provide the rapid-response quotes and technical documentation required for your claim. They can typically provide these services at the preferential rates established in your contract, offering a cost-effective and efficient starting point for the claims process.

Successfully navigating property damage requires a partner that understands both the operational urgency of the repair and the detailed, insurer-grade documentation needed for financial recovery. SnapFixNow bridges this gap. We deliver rapid, warranty-backed repairs and provide the meticulous technical reports essential for supporting your insurance claim. Our ISO-certified process ensures you have the evidence to protect your asset and your bottom line.

Find out how we can help at https://www.SnapFixNow.com.