For facility and asset managers in the UAE, the distinction isn't just semantics—it's a critical financial control. A damage report is an internal, rapid-response tool for operational triage, focused on the 'what' and 'where' to initiate immediate repairs and meet Service Level Agreement (SLA) targets. In contrast, an insurance-ready claim file is a comprehensive, evidence-based dossier engineered for external financial recovery. It must definitively answer the 'why,' 'how,' and 'how much' to satisfy intense insurer scrutiny and protect asset value.

Damage Report vs. Insurance Claim File: An Executive Summary

In Dubai's high-value property market, a critical system failure requires two parallel workflows: immediate operational intervention and meticulous financial justification. Differentiating between a damage report and an insurance-ready claim file directly impacts operational expenditure (OPEX), capital expenditure (CAPEX) planning, and asset protection. One document mobilises the technical team; the other secures the financial reimbursement that safeguards the budget.

This distinction has become even more critical for asset owners and managers. Following recent extreme weather events that led to significant insurer losses across thousands of properties, the capability to produce a robust, insurance-ready claim file has become a key performance indicator for facility management in the UAE. You can find more insights on how these events have shaped the local insurance landscape over on KhaleejTimes.com.

Key Differences at a Glance

A damage report is the first response; a claim file is the financial argument that follows. Each serves a distinct purpose and is built for a different audience. The first is for internal technicians and operations managers; the second is for external loss adjusters, underwriters, and legal teams who demand rigorous, undeniable proof.

The table below breaks down the key differences to help facility, asset, and procurement managers in the UAE make swift, informed decisions.

Key Differences at a Glance Damage Report vs Insurance Claim File

| Attribute | Damage Report (Internal Triage) | Insurance-Ready Claim File (External Recovery) |

|---|---|---|

| Primary Audience | In-house FM team, technicians, supervisors | Insurers, loss adjusters, legal counsel, auditors |

| Core Purpose | Trigger immediate repair, ensure safety, contain damage | Secure financial compensation for loss, justify CAPEX |

| Typical Urgency | Immediate (within 0.5-4 hours) for SLA compliance | Compiled over 7-14 business days for submission |

| Content Focus | What, where, when (e.g., burst pipe, level 3, 02:00) | Why, how, and financial impact (root cause, costings) |

| Evidence Level | Preliminary photos, brief description of issue | Forensic detail, sequential evidence, expert reports |

| Financial Data | Minimal; focus is operational response | Itemised quotes, invoices, proof of payment, cost analysis |

| Decision Supported | "Dispatch a plumbing team now to meet a 2-hour SLA." | "Approve a AED 150,000 claim payment for MEP failure." |

Looking at them side-by-side makes the distinction clear. One is about immediate action to minimise operational disruption, the other about methodical financial recovery to protect the asset's balance sheet value.

A damage report is an operational necessity designed to minimise asset downtime. An insurance-ready claim file is a financial instrument designed to recover capital and protect the balance sheet. Confusing the two can lead to operational delays and rejected claims.

Ultimately, mastering this workflow—from rapid triage to robust financial documentation—is a core competency for modern facility management in the region.

Deconstructing the Damage Report: Its Purpose, Scope, and Limits

In UAE facility management, the damage report is the essential first-response document. Its primary purpose is purely operational: to dispatch a technician immediately, secure the site, and contain the problem. It is the trigger for the entire maintenance workflow.

This document is optimised for speed and clarity, not financial negotiation. It’s designed to capture the critical triage information needed to meet strict Service Level Agreement (SLA) response times, which can range from 30 minutes for critical failures in a hospitality setting to 4 hours for standard issues in a commercial tower. It prioritises action over deep analysis.

Core Components of a Damage Report

A functional damage report contains just enough information to get the right team to the right place with a basic understanding of the situation. The contents are direct, factual, and stripped to the essentials.

- Time and Date Stamps: Precise logs of when the incident was reported and first observed.

- Exact Location Data: Building, floor, specific unit number, or asset tag ID.

- Preliminary Photographic Evidence: Raw, initial photos showing the visible extent of the damage.

- Brief Description: A concise summary of the issue (e.g., "Water ingress from ceiling tiles above server rack, Asset ID: SR-04").

- Technician's Initial Assessment: A first-look evaluation upon arrival, confirming the nature of the problem.

At its core, a damage report is a frontline snapshot. For a burst pipe in a residential community, real-time photos and data logging confirm the urgency for immediate dispatch. This SLA-driven document focuses entirely on triage and can contribute to a reduction in asset downtime by up to 35%—a vital metric in high-occupancy buildings. You can find more insights on the importance of efficient operations in the UAE's service industries.

The Limits of a Damage Report: A Practical Scenario

While vital for operations, a damage report is fundamentally insufficient for financial recovery. Its limitations become clear the moment cost justification is required by an external party like an insurer.

Consider this scenario: A main water pipe bursts on the 15th floor of a JLT commercial tower at 03:00.

- The Damage Report: A security guard logs the issue using a photo-based app. The report contains an image of the flooded corridor, location, and time. It successfully triggers the FM provider's 2-hour emergency SLA, and a plumbing team is dispatched.

- The Operational Success: The team arrives promptly, isolates the water supply, and begins mitigation. Operationally, the damage report fulfilled its purpose as an internal alert.

- The Financial Hurdle: The total repair cost—including pipe replacement, new ceiling tiles, damaged flooring, and specialist drying services—totals AED 30,000. The asset owner decides to file an insurance claim.

The damage report that triggered a AED 500 emergency call-out is not the same document that can justify a AED 30,000 insurance claim. It lacks the three pillars of a successful claim: causation, itemisation, and validation.

The original damage report cannot answer an insurer's key questions. It does not explain why the pipe burst, provide a detailed breakdown of costs from certified vendors, or include a formal engineering assessment. This is the critical gap where a simple report ends and the need for a comprehensive claim file begins.

Building an Insurance-Ready Claim File for Insurer Scrutiny

Transitioning from an internal damage report to a formal, insurance-ready claim file is a significant leap in complexity and purpose. The mindset shifts from operational response to building a persuasive financial argument designed to withstand intense scrutiny from UAE insurers.

This is not a simple folder of documents; it is a structured narrative that proves a covered event occurred and justifies every dirham being claimed. Following major weather events in the region, insurers have heightened their due diligence. They now demand a meticulous evidence trail that leaves no room for ambiguity, particularly regarding common policy exclusions like gradual wear and tear or pre-existing defects.

The Anatomy of a Robust Claim File

To meet these standards, facility managers must go far beyond the initial damage alert. Each component serves a specific purpose, contributing to a cohesive and defensible claim.

- Sequential Photographic and Video Evidence: This is the visual core of the claim. It must include geo-tagged and time-stamped images documenting the asset's condition before the incident (from maintenance logs), during the immediate aftermath (from the initial damage report), and after clean-up and repair work.

- Certified Engineering or Technical Reports: For any significant claim, particularly involving MEP or structural systems (typically exceeding AED 50,000), a third-party report is non-negotiable. This document's function is to definitively establish the root cause of the failure and link it directly to an insured peril, not negligence.

- Itemised Quotations and Invoices: The file must demonstrate procurement diligence. Include at least two to three competitive quotes for the repair work. The final invoice must be equally detailed, breaking down labour, materials, and specialist equipment costs to prove commercial reasonableness.

- Comprehensive Maintenance Logs: These records are the primary defence against a "wear and tear" rejection. A complete history of preventive maintenance demonstrates responsible asset stewardship and helps prove the incident was sudden and accidental.

An insurance-ready claim file transforms raw data into a compelling narrative. It methodically proves that an unforeseen event—a covered peril—was the direct cause of the loss, supported by irrefutable technical and financial evidence.

From Damage Report to Defensible Claim

The process involves enhancing initial data with context, validation, and justification. A basic field alert must be systematically layered with the proof an insurer demands. Using a structured insurance claim form template can serve as a useful starting point to guide information gathering.

The table below outlines the practical steps to convert a simple damage report into a file ready for submission and approval. For a deeper dive, you can also explore our guide on the technical proof your insurer expects.

Checklist for Converting a Damage Report to a Claim File

This checklist shows how to elevate a basic internal report into a dossier that’s ready for an insurer's review. It’s all about adding layers of proof.

| Component | Damage Report (Initial Data) | Claim File (Required Enhancement) | Purpose for Insurer |

|---|---|---|---|

| Evidence | A few photos of the immediate damage. | A full sequential log (before, during, after), including video walkthroughs. | To create an undeniable timeline and counter claims of pre-existing damage. |

| Causation | Brief note, e.g., "pipe leaking." | A certified report detailing failure analysis (e.g., corrosion, pressure surge). | To prove the loss resulted from a covered event, not neglect or gradual decay. |

| Costing | No financial data; focus is on triage. | Multiple itemised quotes, final detailed invoice, proof of payment. | To validate the reasonableness of costs and prevent claim inflation. |

| Asset History | None included. | Complete preventive maintenance records for the affected asset. | To proactively defend against 'wear and tear' or 'poor maintenance' exclusions. |

| Documentation | Single-page internal form. | A compiled dossier with all reports, communication logs, and policy details. | To provide a complete, auditable package for the loss adjuster to review efficiently. |

By meticulously building this evidence-based dossier, facility managers and asset owners in Dubai can navigate the claims process with confidence. It is the necessary approach to ensure recovery of funds needed to protect properties and maintain operational budgets.

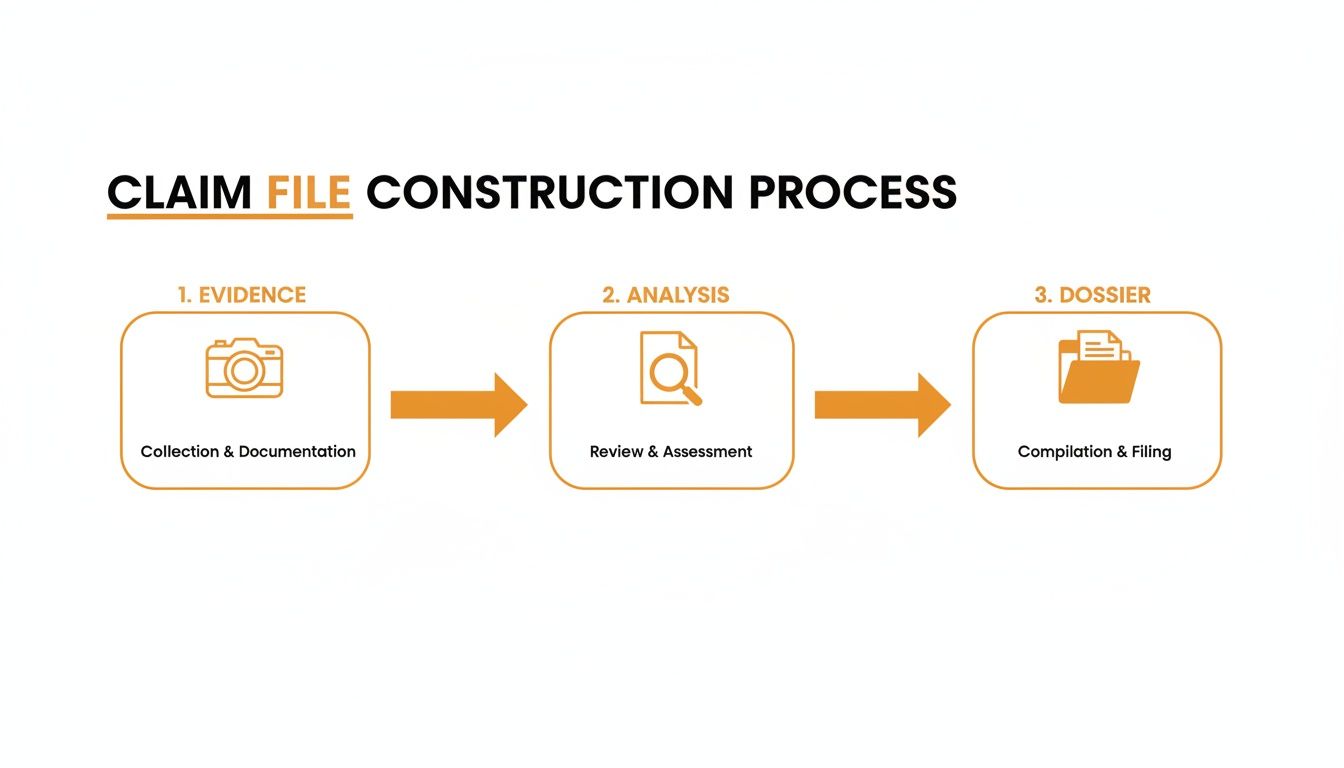

The Strategic Framework for Converting Reports to Claims

Transforming a damage report into an insurance-ready claim file is a strategic process for UAE facility teams. It is a structured workflow designed to convert a costly operational incident into a successful financial recovery. The framework proceeds from initial alert to final submission, ensuring each stage adds a layer of proof that insurers require.

The objective is to build an evidence-based narrative that is difficult to dispute. This requires coordination between on-site technicians, facility managers, procurement teams, and sometimes external specialists. The process is time-sensitive. For a major MEP failure with repair costs exceeding AED 100,000, the team should aim to have the complete claim file ready for submission within 7-10 business days. This timeline is vital for data accuracy and meeting policy notification deadlines, which can be as short as 14 days.

This flow illustrates the essential stages for converting a basic incident alert into a complete claim dossier.

As shown, it is a methodical journey from data capture (Evidence) to technical validation (Analysis) and, finally, organised compilation (Dossier).

Stage 1: Initial Triage and Evidence Capture

This stage begins the moment an incident is logged, typically within minutes of discovery. The focus is on capturing clean, time-stamped evidence before any remedial work begins. The initial damage report serves as the foundation for the claim file.

Key actions include:

- Securing the Site: Ensure the area is safe and prevent further damage.

- Comprehensive Photo and Video Logging: Technicians should capture high-resolution photos and videos from multiple angles, including wide shots for context and close-ups of the failure point.

- Isolating Affected Assets: Document the specific assets damaged—such as a chiller, pump, or electrical panel—ensuring asset tags are visible in the photos.

This phase should be completed within 1-2 hours of the incident report. The quality of evidence gathered here is crucial; poor initial documentation can compromise the entire claim.

Stage 2: Root Cause Analysis and Technical Validation

With immediate evidence secured, the focus shifts from what happened to why it happened. This is the most critical differentiator between a damage report and an insurance-ready claim file. Insurers in the UAE market will reject claims where the cause is ambiguous or suggests neglect or wear and tear.

For any claim exceeding a threshold of approximately AED 50,000, a third-party technical report from a certified engineer is non-negotiable. This independent validation provides the credibility needed to prove the incident was a sudden and unforeseen event covered by the policy.

The analysis must pinpoint a specific root cause, such as a manufacturing defect, a sudden pressure surge, or external impact. The report must explicitly rule out gradual deterioration as the primary cause of failure. This stage typically takes 3-5 business days, depending on system complexity and specialist availability.

Stage 3: Procurement and Detailed Costing

Once the cause is established, the next step is to accurately quantify the financial loss. A single invoice is insufficient for a significant claim. Insurers require proof that repair costs are fair, competitive, and directly attributable to the insured event.

This entails a formal procurement process:

- Develop a Detailed Scope of Work: Create a precise brief outlining all required repairs.

- Obtain Multiple Quotations: Secure at least three itemised quotes from reputable, licensed vendors.

- Analyse and Select a Vendor: Document the rationale for contractor selection, based on price, capability, and timeline.

The submission must include all received quotes, the final detailed invoice, and proof of payment. This demonstrates due diligence and prevents insurers from claiming costs were inflated. This phase should run concurrently with the root cause analysis and typically takes 4-6 business days.

Stage 4: Structured Documentation Collation

The final stage involves assembling all information into an organised dossier. The initial damage report is fully integrated into this comprehensive package. The file must be structured logically for easy review by an adjuster, beginning with a clear cover letter summarising the event, cause, and total claimed amount.

This final dossier transforms an operational alert into a compelling financial argument, built on a foundation of technical proof and procedural discipline.

Navigating Common Claim Pitfalls in the UAE Market

Securing claim approval in the UAE involves navigating a landscape of potential procedural and evidentiary traps. Local insurers adhere to exceptionally high documentation standards. Minor oversights can lead to significant delays or outright rejection. For property and facility managers, understanding these common mistakes is the first step to avoiding them.

This is where the difference between a damage report and an insurance-ready claim file becomes most apparent. A brief notification of a malfunction is insufficient. Insurers require a compelling, evidence-backed dossier that proves a covered event occurred and that all due diligence was performed beforehand.

Failure to Prove Causation Over Neglect

One of the most frequent reasons for claim denial is the failure to distinguish between a sudden, insured event and gradual deterioration from neglect. In cases of ambiguity, insurers often invoke the "wear and tear" exclusion.

- The Pitfall: A claim for a failed HVAC chiller is submitted with only a few photos of the breakdown. The insurer argues the failure was due to age and inadequate servicing over time—a non-covered cause.

- The Solution: The claim file must include a third-party engineering report identifying a specific, sudden cause, like an electrical surge or a critical component failure. This must be supported by at least 12-24 months of preventive maintenance logs showing the unit was serviced according to manufacturer specifications. This evidence shifts the narrative from neglect to an unforeseen accident.

Incomplete or Disjointed Photographic Evidence

A few photos taken immediately after an incident are insufficient. Insurers require a clear, chronological visual narrative that eliminates doubt about the asset's condition before the damage.

An incomplete photo log is an open invitation for an insurer to question the timeline and extent of the damage. Without 'before' photos from asset condition logs, it becomes your word against theirs regarding the state of the asset prior to the incident.

A robust visual file should always include:

- 'Before' Photos: Pulled from recent maintenance reports or digital asset logs.

- 'During' Photos: Captured immediately after the incident to show the raw damage.

- 'After' Photos: Documenting the completed repairs to show the restored condition.

Misinterpreting Policy Exclusions

Many UAE property insurance policies contain specific exclusions for gradual damage, such as slow leaks, corrosion, or mould. If a claim file inadvertently describes a problem as ongoing or developing over time, it provides the insurer with grounds for rejection.

- The Pitfall: A technician’s report mentions "a long-term seepage issue" when describing water damage. This wording is a red flag that directly triggers the gradual damage exclusion clause.

- The Solution: Train staff to document facts, not interpretations. The report should state, "Water damage discovered on [Date] originating from a burst pipe in unit X." The entire focus must be on the sudden event (the pipe bursting), not the resulting damage that may have taken time to become apparent. You can learn more about common reasons for claim denials and why property insurance claims get delayed or rejected in Dubai.

By anticipating these challenges, facility managers can build a more proactive and resilient claims strategy. It comes down to meticulous records, precise language, and a deep understanding of what local insurers need to see. This approach transforms a claim from a simple request into a well-defended financial argument, significantly improving the probability of approval.

Using Technology for Seamless Claim Documentation

Modern facility management platforms provide the critical bridge between an initial damage report and an insurance-ready claim file. Technology transforms a traditionally manual, paper-intensive process into a streamlined, data-driven workflow. This is especially valuable for property managers in Dubai, where speed of response and accuracy of documentation are equally non-negotiable.

Photo-based work order systems create an immutable, time-stamped audit trail from the moment an incident is logged. This digital chain of custody provides the undeniable evidence that UAE insurers demand, replacing ambiguous handwritten notes with clear, objective data captured in real-time.

Streamlining the Evidence-Gathering Process

The right technology empowers on-site engineering teams to become expert evidence collectors without distracting from their primary task of problem resolution. Key features are designed to support the creation of a robust, insurance-ready file from the outset.

These capabilities include:

- Real-time Photo and Video Uploads: Technicians capture photos and videos at the site, which are instantly geo-tagged and time-stamped, creating a verifiable record of the damage as it was discovered.

- Automated Report Generation: Platforms can automatically generate initial damage reports, populating them with critical data—location, time, photos, and initial notes—to ensure completeness.

- Digital Asset Histories: A complete digital log of all maintenance for every asset allows for the instant retrieval of service records, which is the best defence against a claim of neglect or "wear and tear."

- Centralised Document Storage: All related documents, from third-party engineering reports to vendor quotations and final invoices, are stored in a single, accessible digital folder tied to the specific incident.

Technology transforms claim documentation from a reactive, administrative burden into a proactive, integrated part of the maintenance workflow. This ensures that every work order for a potential claim is captured with insurer-grade detail from the very first minute.

Beyond data capture, advanced tools can assist with subsequent administrative tasks. For example, efficient AI PDF summarizer tools can help teams quickly extract key findings from lengthy engineering reports or dense policy documents, saving significant time during claim preparation.

This technology-first approach not only reduces the administrative burden on facility managers but also significantly increases the probability of a successful insurance claim. By embedding documentation best practices into daily operations, organisations can protect their OPEX and safeguard long-term asset value. You can learn more about adopting a modern approach in our guide to technology-enabled maintenance solutions.

Frequently Asked Questions

For facility and property managers in the UAE, several key questions consistently arise when dealing with property damage and insurance claims. Here are clear, practical answers that clarify the difference between a damage report and an insurance-ready claim file.

How Long Do I Have to File an Insurance Claim in the UAE?

Most UAE property insurance policies operate on a strict two-step timeline. The first is immediate notification. Policyholders are typically required to inform the insurer of a potential loss within 7 to 14 days of the incident. This initial notification is crucial and is usually triggered by your internal damage report.

Following this notice, a separate, longer deadline exists for submitting the complete, evidence-based claim file. However, missing the initial notification window can invalidate the entire claim, regardless of the quality of the final documentation. Always review the specific notification clause in your policy.

Can I Use My In-House Team Report for an Insurance Claim?

An in-house damage report is an essential starting point and provides vital initial evidence. For smaller claims, typically those under AED 20,000, it may be sufficient if it includes clear photos and a concise description of the incident.

However, for significant claims involving major MEP failures, structural issues, or extensive water damage, insurers will almost certainly require a supplementary report from a certified, independent third-party engineer or specialist. The in-house report establishes the timeline, but external validation provides the unbiased, expert analysis of causation that insurers need to approve a substantial payment.

Your internal report is the first chapter, proving the 'when' and 'what'. A third-party report is the expert analysis that proves the 'why'—the cornerstone of a successful claim.

What Is a Common Reason for Claim Rejections in Dubai?

A leading cause for claim rejections in the Dubai and wider UAE market is the failure to definitively prove a covered "insured peril" (e.g., a sudden storm, abrupt mechanical failure) as opposed to a non-covered issue. The most common grounds for rejection are "gradual wear and tear" or damage attributed to poor maintenance.

A successful claim file must construct a clear, evidence-based argument for a sudden and unforeseen event. The most effective way to achieve this is by presenting consistent preventive maintenance records alongside a technical report that pinpoints a specific moment of failure. Without this proof, insurers can easily default to a position of owner neglect.

Are Photos Enough Evidence for an Insurance Claim?

Photos are critical but are never sufficient on their own. They provide powerful visual proof but lack the context and complete narrative required for an insurance-ready claim file. A loss adjuster needs the complete package to make a decision.

This package must include:

- Detailed technical reports explaining the root cause of the damage.

- Itemised invoices and quotations to justify the financial loss.

- Preventive maintenance logs to demonstrate due diligence.

- Official correspondence between all involved parties.

Think of photos as evidence that supports the narrative, but does not replace it. High-quality, time-stamped video is even more effective for providing a dynamic view of the damage and its immediate aftermath.

At SnapFixNow, we understand that the gap between a simple report and a complete claim file can determine the financial outcome of a major incident. Our photo-based work order platform and expert technical teams help you build a robust, evidence-backed dossier from the moment damage is detected, ensuring you have the documentation needed to protect your assets. Learn more about our engineering-led facility management services at https://www.SnapFixNow.com.