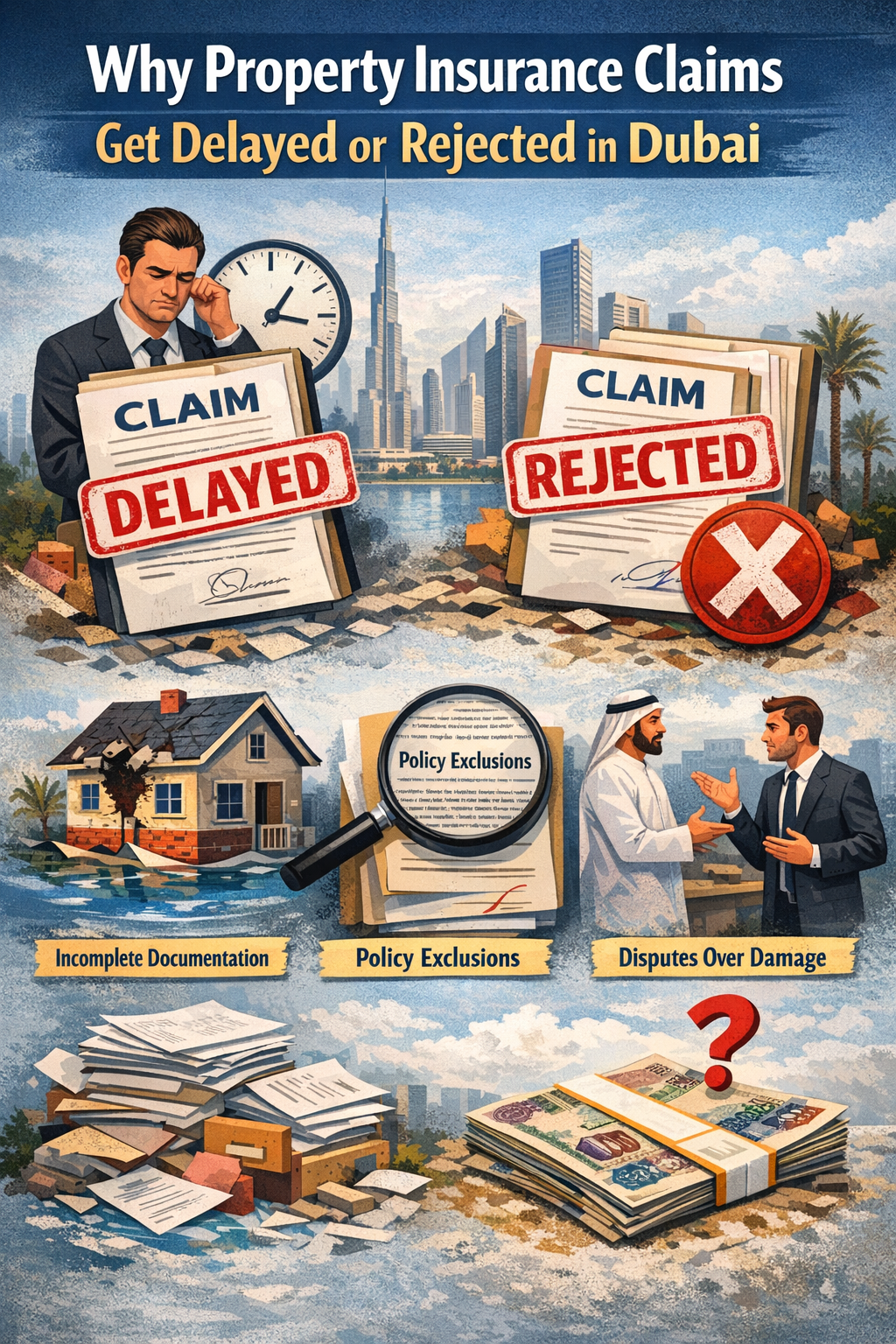

Property insurance claims in Dubai are often delayed or partially rejected not because the damage is invalid, but because the claim file lacks the technical and procedural clarity insurers and loss adjusters require.

For commercial buildings, offices, retail units, and hospitality assets, insurance claims typically fall under Business All Risk (BAR) or comprehensive property policies. These policies are technical by nature, and insurers assess them based on evidence, causation, policy conditions, and compliance, not intent alone.

1. Incomplete or Poor Documentation

One of the most frequent causes of claim delays is insufficient or unstructured documentation. Common issues include photos without timestamps or scale reference, videos that show damage but not the cause, missing records of pre-damage condition, and the absence of a clear incident timeline.

Insurers and loss adjusters generally expect documentation that answers three questions clearly: What failed? Why did it fail? What assets were affected as a result?

2. No Clear Identification of Root Cause

Insurance coverage is triggered by insured causes of loss, not by damage alone. For example, sudden pipe rupture may be covered, whereas long-term seepage or corrosion may not be. Many claims fail because they focus on visible damage without technically establishing the root cause. Engineering-led assessment is critical at this stage.

3. Misunderstanding the Role of the Loss Adjuster

A common misconception is that the loss adjuster acts on behalf of the policyholder. In reality, the loss adjuster is an independent investigator appointed by the insurer. Their role is to assess cause, extent, and policy applicability—not to advocate for either party. Managing this relationship professionally through clear documentation and factual reporting is key.

4. Repairs Undertaken Before Proper Assessment

While quick restoration is often necessary, premature permanent repairs can complicate claims. Most policies include a Duty of Mitigation, requiring reasonable steps to prevent further damage. Acceptable mitigation actions include stopping active leaks, isolating power, or securing openings. The key is documenting mitigation actions while deferring permanent rectification until assessment is complete.

5. Contractor Quotes Without a Technical Narrative

Contractor repair quotations typically describe what needs to be fixed but do not explain why the damage occurred or link it to an insured event. From an insurer’s perspective, a quote is a cost estimate—not claim justification.

6. Misalignment With Policy Terms and Conditions

Insurance policies define covered perils, exclusions, limits, and conditions such as mitigation and notification requirements. Claims are often delayed when the incident description does not align clearly with policy wording. This requires technical interpretation rather than general reporting.

How Professional Claim Support Improves Outcomes

Specialized facility management companies such as SnapFixNow™ FMC support insurance claims by providing engineering-led documentation, including technical damage assessment, root cause analysis, evidence capture, timeline documentation, and claim-ready reporting aligned with insurer expectations.

Dispute Resolution (When Required)

In rare cases where claims remain unresolved despite proper documentation, policyholders may explore formal escalation channels. In the UAE, insurance oversight and dispute escalation mechanisms fall under the Central Bank of the UAE, which regulates insurance activities previously overseen by the Insurance Authority.

Final Thought

Most insurance claim challenges in Dubai arise from process gaps, not lack of coverage. With proper documentation, technical clarity, and structured mitigation, many delays and disputes can be avoided.